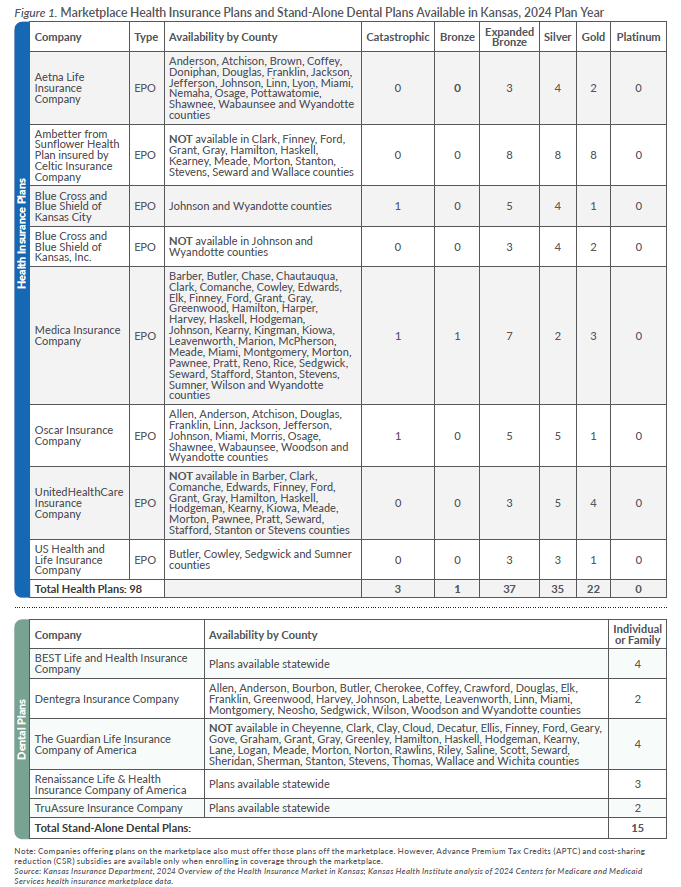

The reduction in the number of health plans available on the Kansas marketplace for 2024 is due, in part, to Cigna Health and Life Insurance Company, which offered 25 plans across eight counties in 2023, choosing not to offer plans in Kansas for 2024. Aetna Life Insurance Company, new to the Kansas marketplace for 2024, is offering only nine plans across 19 counties.

All eight insurers are offering expanded bronze, silver and gold plans. One insurer is offering a bronze plan, and three insurers are also offering catastrophic plans. For the seventh consecutive year, there are no platinum plans being offered to individuals on the Kansas marketplace. Like in 2023, all counties in Kansas have at least two insurers offering coverage and all plans offered are exclusive provider organization (EPO) plans, which only cover services provided in-network by a “narrow network” of providers, except in an emergency.

Under the ACA, dental coverage is an essential health benefit for children enrolled in an ACA-compliant health plan and is included in the premium cost, but not for adults.

Some insurers offer policies with both health and dental coverage for adults, meaning the premium covers both health and dental policies and APTC can be applied.

Alternatively, adults can purchase a stand-alone dental plan, but they also must be enrolled in an ACA-compliant health plan and will be responsible for two separate premiums. APTC cannot be applied to stand-alone dental plan premiums. There are a total of 15 stand-alone dental plans available from five insurers for 2024.