Introduction

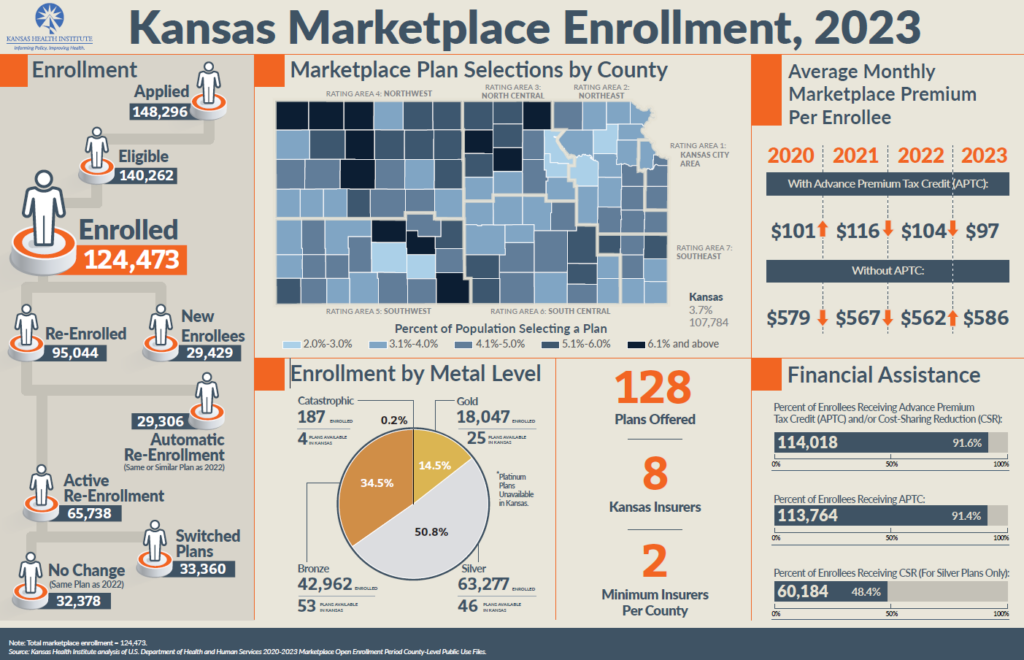

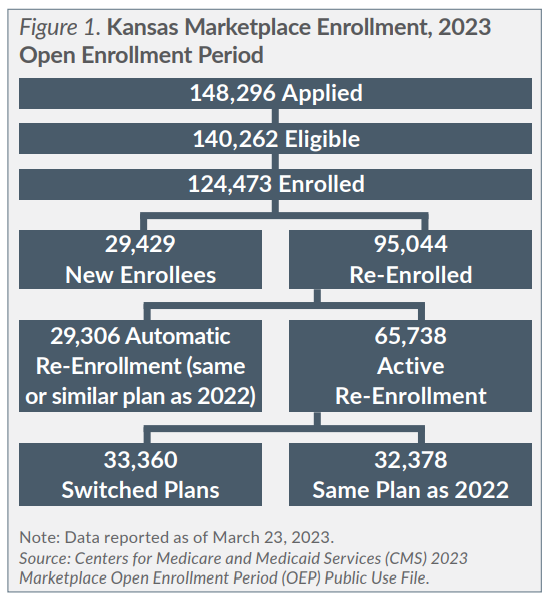

During the 2023 plan year open enrollment period (OEP) that ended Jan. 15, 2023, a record 124,473 Kansans selected or were automatically re-enrolled in a health insurance plan through the federally facilitated marketplace — an increase of 16,689 (15.5 percent) compared to last year’s record high enrollment. In the United States, 16.4 million consumers enrolled during the 2023 OEP, which is also about a 12.7 percent increase from 14.5 million the previous year and is also a record enrollment for the marketplace nationally. The 2023 OEP was the second OEP since the American Rescue Plan Act of 2021 (ARPA) to increase the value of Advance Premium Tax Credits (APTC) and make them available to more enrollees.

This brief provides summary data from the 2023 OEP on enrollment, enrollee characteristics, plan selection, financial assistance, premiums and stand-alone dental insurance in Kansas. Like last year, the OEP lasted 75 days, from Nov. 1, 2022, through Jan. 15, 2023. Coverage began Jan. 1, 2023, for those who enrolled on or before Dec. 15 and began on Feb. 1 for those who enrolled after Dec. 15.