Introduction

The tenth annual open enrollment period (OEP) for the Kansas health insurance marketplace, created by the Affordable Care Act (ACA) and operated by the federal government through Healthcare.gov, began on Nov. 1, 2022, and ended Jan. 15, 2023. While the OEP for plan years 2018 through 2021 lasted only 45 days, from Nov. 1 through Dec. 15, the Centers for Medicare and Medicaid Services (CMS) announced in September 2021 that starting with plan year 2022, the OEP would begin running from Nov. 1 through Jan. 15 to provide consumers with an additional 30 days to review and sign up for coverage. For plan year 2023, coverage for individuals who enrolled by Dec. 15 became effective Jan. 1, 2023. Coverage for individuals who enrolled after Dec. 15 but by Jan. 15 became effective on Feb. 1, 2023.

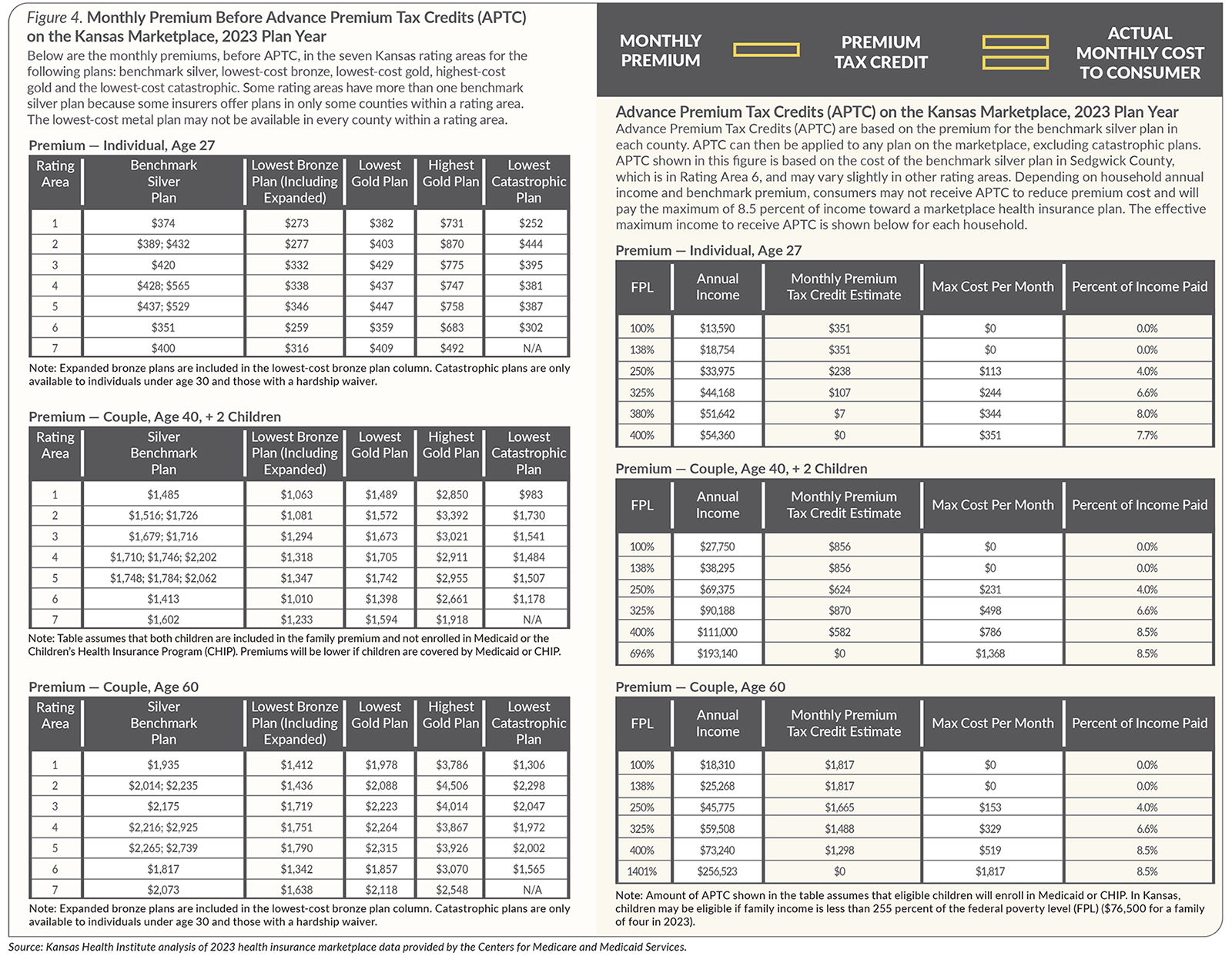

For plan year 2023, the Inflation Reduction Act of 2022 makes it possible for individuals enrolling for plan year 2023 to continue to benefit from the enhanced Advance Premium Tax Credits (APTC) made available in 2022 through the American Rescue Plan Act of 2021 (ARPA). The Inflation Reduction Act extends the temporary enhancements of the ARPA through plan year 2025.

Prior to 2023, an estimated 40,000 Kansans were not eligible to receive premium tax credits due to what was known as the “family glitch.” The “family glitch” refers to a 2013 ACA implementation rule that applied to families of individuals with employer-sponsored insurance to determine whether the cost of the coverage was affordable, thereby making the employee and their family ineligible for APTC to purchase coverage on the marketplace. Under this rule, coverage was considered affordable based solely on the cost of only the employee’s premium, even if premiums for the whole family were not affordable. In 2022, prior to the start of the 2023 OEP, the Biden administration and the Internal Revenue Service finalized a rule to address the family glitch to allow the cost of family premiums to be used to determine affordability, thereby potentially making more spouses and children eligible for APTC to purchase coverage on the marketplace.

This brief provides information about plan options offered for the 2023 plan year, health insurance costs, financial assistance options and factors impacting enrollment.