Factors Impacting Enrollment on the ACA Marketplace

For 2025, several factors may impact enrollment, including those listed below.

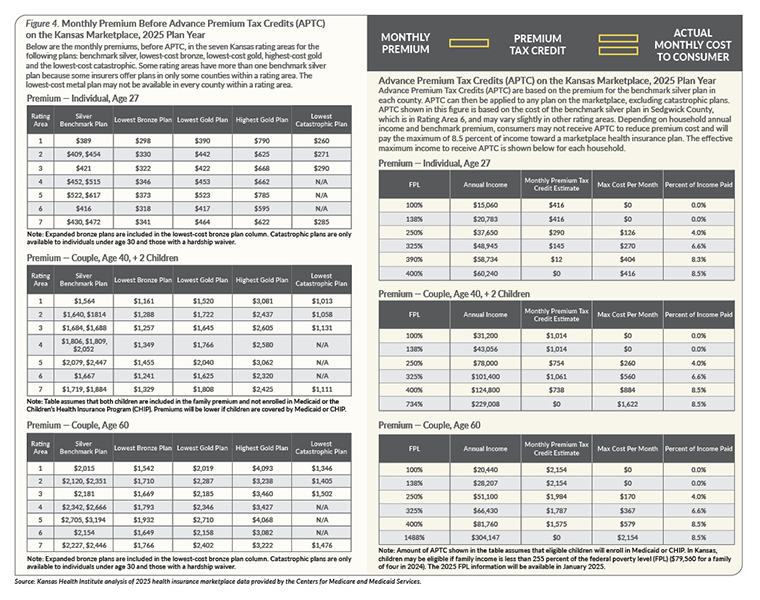

Continuation of the enhanced APTC provided in the ARPA and the IRA through 2025 could lead to a fourth record year of enrollment.

The Special Enrollment Period continues throughout plan year 2025 for consumers with household income up to 150 percent FPL ($22,590 for an individual and $46,800 for a family of four) that are eligible for APTC. In Kansas, most individuals below 100 percent FPL do not qualify for APTC on the marketplace.

The percentage for determining affordability of employer-sponsored health coverage under the ACA is 9.02 percent, which is higher than the 8.39 percent in 2024, but lower than the 9.12 percent in plan year 2023. The increased threshold for affordable employer coverage reduces the number of families that are able to seek marketplace plans with subsidies.

A Final Rule issued by the U.S. Department of Health and Human Services (HHS) in May 2024 made Deferred Action for Childhood Arrivals (DACA) recipients eligible to sign up for coverage through the marketplace as of Nov. 1, 2024, with coverage beginning as early as Dec. 1, 2024. Under the rule, DACA enrollees also were given access to APTC and CSR, even if their income is below 100 percent FPL. CMS estimated that the new rule could provide coverage to approximately 100,000 DACA recipients nationwide who are currently uninsured. However, in August 2024, 19 states, led by Kansas Attorney General Kris Kobach, filed a lawsuit in North Dakota federal court challenging the HHS rule and seeking to invalidate it. On Dec. 9, the court granted the states’ motion for a preliminary injunction and a stay to the Final Rule, which preliminarily prohibits enforcement of the rule in those states.