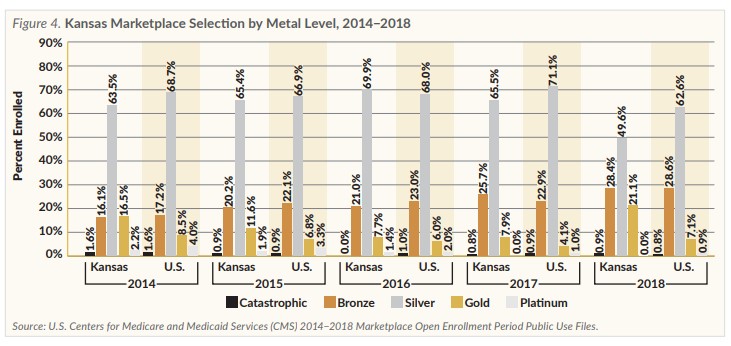

Another change has been the different types of plans offered by insurers under the metal tiers, including preferred provider organization (PPO) plans, health maintenance organization (HMO) plans and exclusive provider organization (EPO) plans. PPO plans typically have a network of “preferred” providers that enrollees are encouraged to use, but the plans also will pay a reduced amount for out-of-network care. HMO plans tend to have lower monthly premiums and lower cost-sharing than PPOs, but they might require enrollees to obtain referrals from their primary care provider for specialty care services. They also might not pay for out-of-network care except in emergencies. EPO plans have a network of “exclusive” providers that enrollees must use for their care or the plan will not pay.

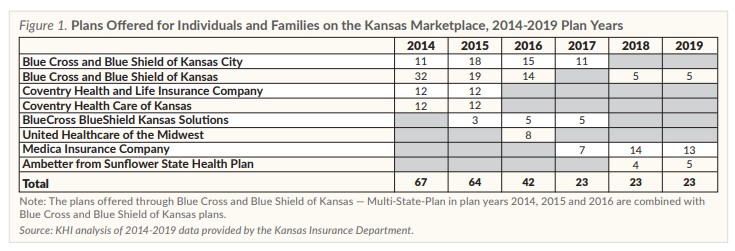

In 2014, 67 plans were offered for individuals and families by four companies: Blue Cross and Blue Shield of Kansas (BCBSKS) offered PPO plans in all Kansas counties except Johnson and Wyandotte; Blue Cross and Blue Shield of Kansas City (BCBSKC) offered PPO plans only in Johnson and Wyandotte counties; Coventry Health Care of Kansas offered HMO plans only; and Coventry Health and Life Insurance offered PPO plans only. Both Coventry companies offered coverage in all 105 Kansas counties, but they ended their participation in the marketplace at the end of 2015. For plan year 2015, 64 plans were offered by five companies, and in plan year 2016, 42 plans were offered by four companies.

Beginning with plan year 2017, the total number of plans offered on the Kansas marketplace dropped to 23, and the number of companies offering coverage in Kansas fell to three — BlueCross BlueShield Kansas Solutions, Blue Cross and Blue Shield of Kansas City and Medica Insurance Company, a new entrant into the Kansas health insurance market. None of the companies offered platinum plans, and Blue Cross and Blue Shield of Kansas elected not to offer coverage on the marketplace at all for 2017.

In 2018, the Kansas marketplace included 23 health plans offered by three companies. BCBSKS returned to the Kansas marketplace, offering only EPO plans in all counties except Johnson and Wyandotte, while Medica offered PPO plans in all counties except Johnson and Wyandotte and EPO plans in Johnson and Wyandotte. Ambetter from Sunflower State Health Plan, a new insurer on the marketplace, offered only HMO plans in Johnson and Wyandotte counties.

For plan year 2019, three companies — BCBSKS, Medica and Ambetter from Sunflower State Health Plan — are offering 23 plans on the Kansas marketplace, including EPO and HMO plan types. There are at least two companies selling plans in each Kansas county. There aren’t any PPO plans or platinum level plans.

Premiums and Financial Assistance

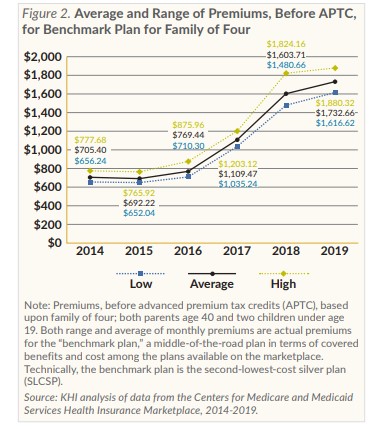

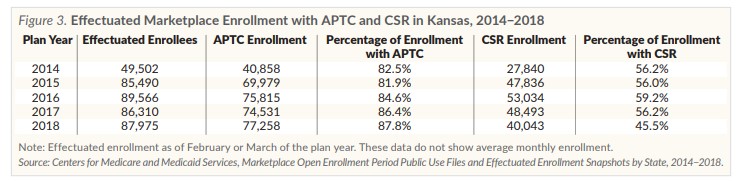

Under the ACA, individuals with annual incomes between 100 and 400 percent of the federal poverty level (FPL) may be eligible for advanced premium tax credits (APTC) to help pay premiums. Individuals with incomes between 100 and 250 percent of FPL also may be eligible for cost-sharing reduction (CSR) subsidies, which reduce their out-of-pocket costs (deductibles, co-payments and coinsurance) when using their insurance. The APTC is calculated using the cost of the “benchmark plan,” or second-lowest cost silver plan in each state, and varies based on the individual’s income, age and family size. However, once the amount of the APTC has been calculated, consumers may use it to purchase a bronze, silver or gold plan.

For plan year 2014, monthly premiums for the silver “benchmark” plan across the state for a family of four (both parents age 40 with two children under age 19) ranged from $656 to $778 (Figure 2). For 2015, the benchmark plan premiums ranged from $652 to $766 for a family of four.