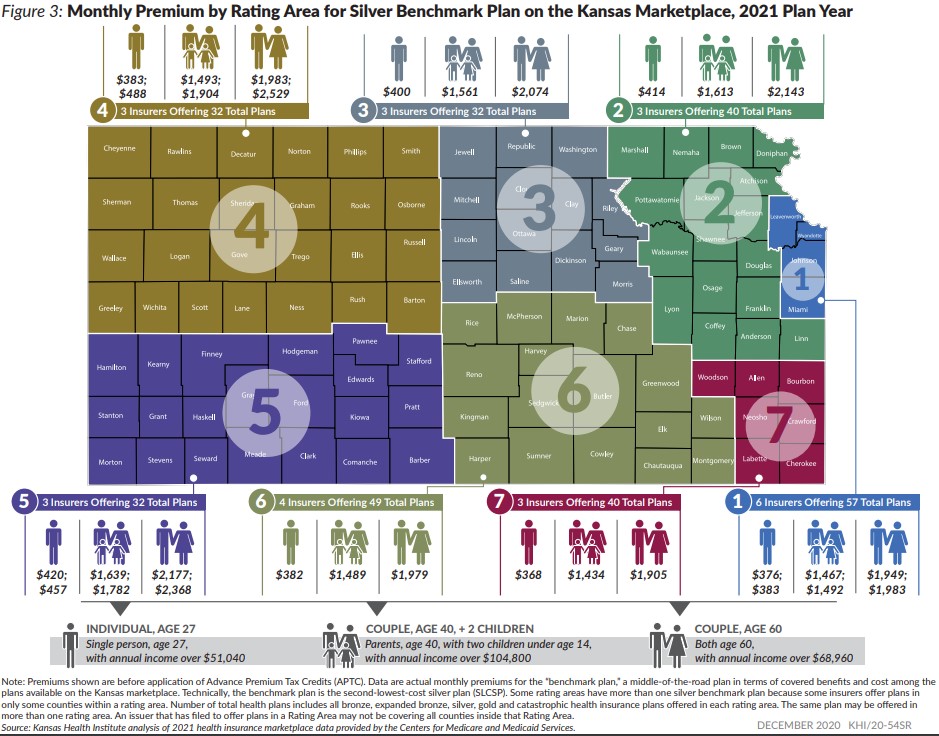

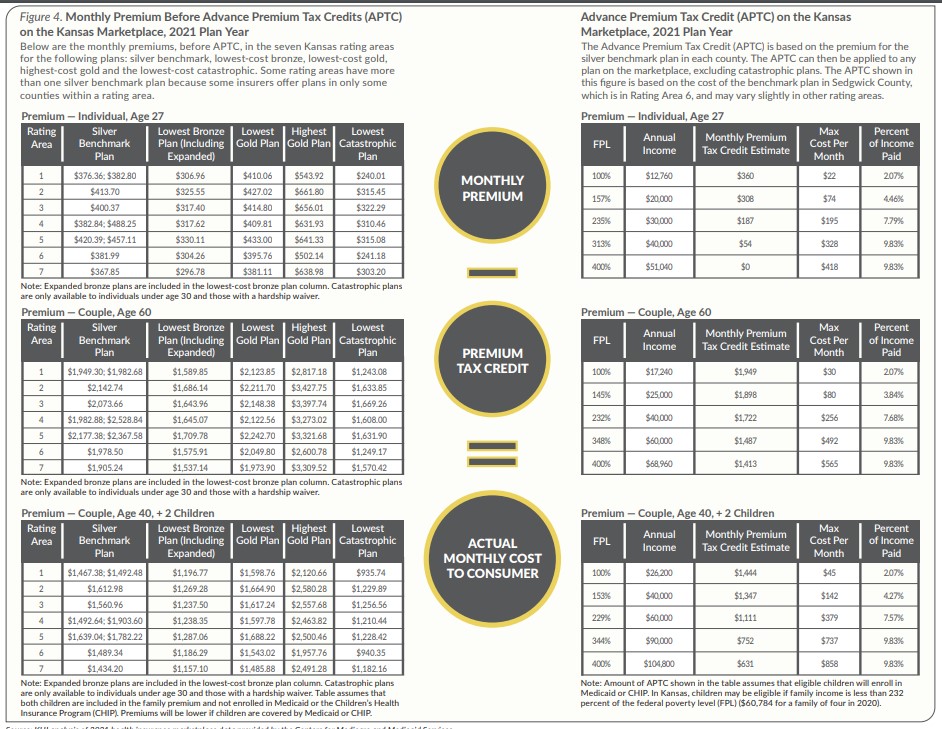

APTC are based on the cost of the benchmark plan but may be used to purchase any metal-level plan available on the marketplace. With APTC, consumers could be better off with a more benefit-rich gold plan with a lower deductible. For example, a gold plan in Sedgwick County could have a monthly premium of $396 before APTC (or $209 after APTC) and a deductible of $750 for an individual with household income of 235 percent FPL. In comparison, the same individual could purchase a silver plan with a slightly lower monthly premium of $382 before APTC (or $195 after APTC) but would have a higher deductible of $3,300.

Consumers with household income between 100 and 250 percent of FPL ($26,200 to $65,500 for a family of four in 2020) who enroll in silver plans may be eligible for cost-sharing reduction (CSR) subsidies to lower their out-of-pocket expenses. CSR is not available with any other metal-level. For example, the deductible could be lowered to $0 with reduced co-payment/co-insurance for a benchmark plan for enrollees in Sedgwick County with income between 100 and 200 percent FPL.

Factors Impacting Enrollment on the ACA Marketplace

While the cost of coverage is a barrier to enrollment for many consumers shopping on the ACA marketplace, low health insurance literacy and the emergence of non-ACA-compliant plans might also impact enrollment.

Reduced Navigator Funding. Under the ACA, the federal government is required to provide funding to states using Healthcare.gov to establish navigator programs for outreach and education for consumers who are interested in purchasing coverage on the marketplace. For plan years 2020 and 2021, two Kansas organizations received $213,317 to serve 17 counties throughout Northeast, Central and Western Kansas, which is down from $312,260 received by two organizations serving all 105 Kansas counties in 2019.

Emergence of Non-ACA-Compliant Plans. Non-ACA-compliant plans have gained more traction following elimination of the individual mandate penalty in 2019. These plans are not required to meet the ACA health insurance requirements and therefore can deny coverage to individuals with pre-existing conditions and exclude some essential health benefits. These plans often are less expensive, which makes them attractive to healthy consumers and could lead to instability on the ACA marketplace.

Examples of non-ACA-compliant plans available to individuals and families are short-term limited duration insurance, health benefits plans and health care sharing ministries.

Short-Term Limited Duration Insurance (STLDI) is a type of health insurance originally designed to allow consumers to fill temporary gaps in coverage for short periods of time. However, in 2018, the Trump administration issued a federal rule extending the permissible terms of these policies to up to 364 days. Kansas law (K.S.A. 40-12,193) limits terms to six or 12 months based upon policy design. In November 2020, KID reported eight companies which may offer STLDI policies in Kansas.

Health Benefits Plans, such as those offered by the Kansas Farm Bureau (KFB) starting October 2019, pay a set amount of money when a consumer experiences a medical event. These plans are not considered health insurance and are therefore exempt from state insurance regulation. KFB reports that their membership consists of more than 30,000 farmers and ranchers in Kansas but estimates of how many members had actually purchased the health benefit were not available.

Health Care Sharing Ministries (HCSM) are arrangements in which members who follow a common set of religious or ethical beliefs agree to contribute regular payments (similar to premiums) toward qualifying medical expenses of the group and also must pay some out-of-pocket costs. HCSMs are not considered health insurance and are therefore exempt from state insurance regulation in Kansas. A recently proposed IRS Rule that would allow individuals who participate in HCSMs to deduct the amounts paid as medical expenses may encourage more individuals to join these types of arrangements. The Alliance of Health Care Sharing Ministries reported that there are 19,184 active Kansas members in 2020.

Looking Ahead

Many factors could impact 2021 open enrollment. The addition of more plans and insurers, decreasing premiums and the ongoing COVID-19 pandemic could be expected to increase enrollment for the 2021 plan year. However, less expensive non-ACA-compliant plans may lead some consumers away from the marketplace. There also could be some concern about the future of the marketplace as the U.S. Supreme Court considers California v. Texas, in which 20 states including Kansas are challenging the validity of the entire ACA law after the elimination of the individual mandate penalty.