Employment

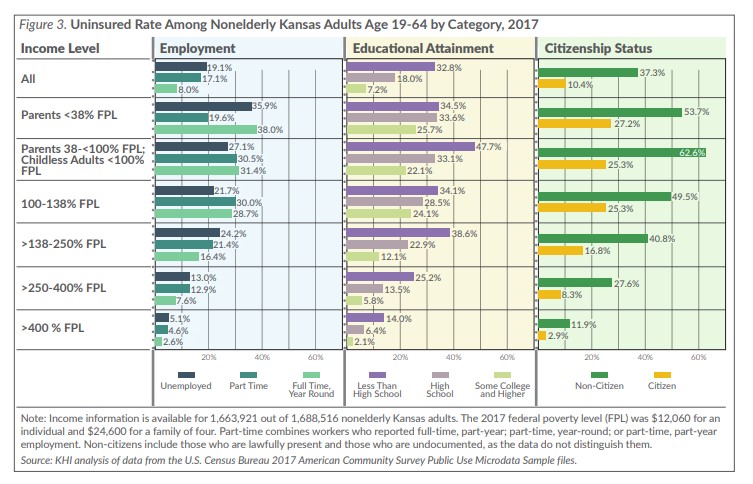

Overall, unemployed individuals were 2.4 times more likely to be uninsured than were those who worked full-time year-round (19.1 percent compared to 8.0 percent; Figure 3). However, among those with family income less than 138 percent FPL, the uninsured rate was not better for those employed full-time year-round compared to those who were unemployed (the small differences shown were not statistically significant). This raises important questions about the often-cited assumption that obtaining low-wage employment — even if it is full-time year-round — is a good way to get insurance coverage. For those with family income over 138 percent FPL, unemployed individuals were 1.5 to 2 times more likely to be uninsured than were those who worked full-time year-round. This suggests that for better paying jobs, the benefit of full-time employment related to gaining insurance coverage holds true.

Education

Individuals with less than a high school education were 4.6 times more likely to be uninsured than were those with some college education or higher (32.8 percent compared to 7.2 percent; Figure 3). For nonelderly adults whose family income was >400 percent FPL, those who had not completed high school were 6.7 times more likely to be uninsured than were those who had completed some college or higher (14.0 percent compared to 2.1 percent).

Citizenship

Nonelderly adults who were not U.S. citizens were 3.6 times (37.3 percent compared to 10.4 percent) more likely to be uninsured than were U.S. citizens (Figure 3). The difference ranged from 2.0 times (49.5 percent compared to 25.3 percent) more likely for uninsured nonelderly adults with family income 100-138 percent FPL to 4.1 times (11.9 percent compared to 2.9 percent) more likely among those with income >400 percent FPL.

Discussion and Conclusions

Approximately 200,000 nonelderly Kansas adults were uninsured in 2017, despite existing coverage options and financial assistance. Although most (73.4 percent) were working, they might have worked for an employer that did not offer health insurance, they could not afford premiums or out-of-pocket expenses, or they worked part-time and were ineligible for coverage. Targeted outreach efforts could help some of these working individuals gain coverage; however, several groups of uninsured nonelderly adults still face barriers to coverage.

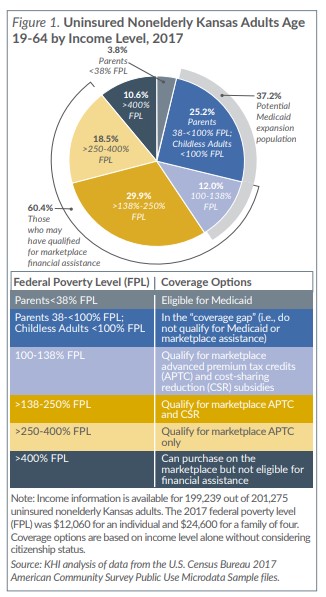

One in four (25.2 percent) uninsured nonelderly Kansas adults were parents with family income 38-<100 percent FPL or childless individuals with income <100 percent FPL. They fell into the “coverage gap,” in which their income is too low to qualify for marketplace financial assistance and they were not eligible for Medicaid, unless expanded.

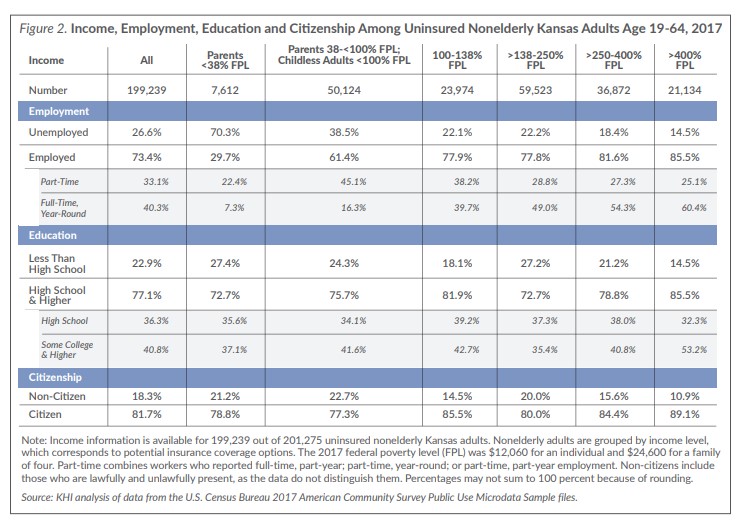

Nearly one in five (18.3 percent) uninsured nonelderly Kansas adults were not U.S. citizens, a group that includes those here legally and illegally. Undocumented immigrants are not eligible for Medicaid and cannot purchase marketplace plans. Lawfully present immigrants can purchase marketplace plans and qualify for financial assistance, and while eligible for Medicaid or CHIP in Kansas, there is a five-year waiting period. As of January 2019, 33 states and Washington, D.C., have waived the waiting period for immigrant children and 24 states and Washington, D.C., have waived it for pregnant women. Kansas has not waived the waiting period for either group. Some states also have state-funded health care programs for noncitizens regardless of immigration status.

During the 2019 Kansas legislative session, several bills focused on the eligibility and affordability of health insurance, including House Bills (HB) 2209 and 2066.

-

- House Bill 2209 allowed the Kansas Farm Bureau to sell health care benefits that are not considered insurance and will not be regulated by the Kansas Insurance Department. It also amended Kansas law regulating association health plans, which may expand the use of these plans in the future. HB 2209 became law without Governor Kelly’s signature.

- House Bill 2066 would have expanded Medicaid eligibility to nonelderly Kansas adults with income up to 138 percent FPL. The bill was passed by the House but remained in the Senate Public Health and Welfare Committee. Attempts to pull the bill out of committee and place it on the Senate calendar for a vote failed

Although additional strategies for increasing health insurance coverage have been introduced, concerns have been raised in several areas, such as consumer protection, the loss of healthy individuals from the ACA compliant individual and small group markets, and the cost to the state. While the overall effects of Medicaid expansion in Kansas have been estimated, including the number of enrollees and projected cost to the state, the effects of HB 2209 on health insurance coverage and on the health insurance market itself have not been examined. Continued monitoring of changes in the uninsured rate and the health insurance market in Kansas is warranted.