Introduction

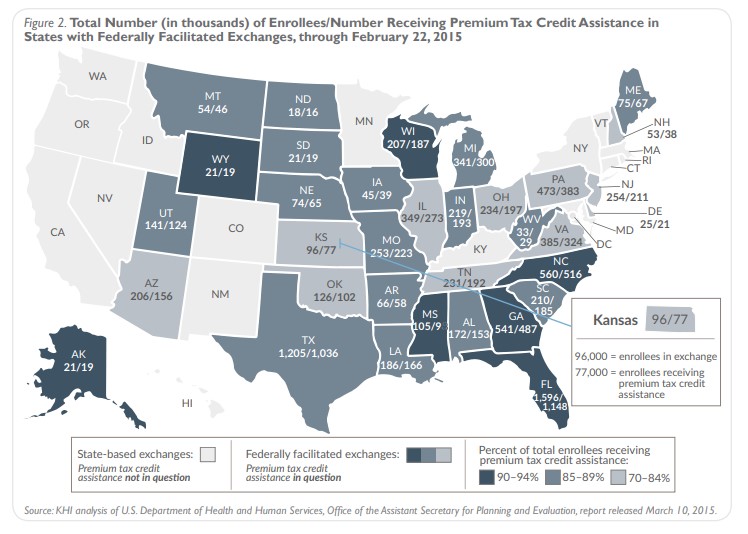

On Wednesday, March 4, 2015, the U.S. Supreme Court heard 90 minutes of oral argument in the case of King v. Burwell, which questions the validity of the Internal Revenue Service (IRS) regulation that allows eligible individuals who purchase health insurance through an exchange established by the federal government to receive premium tax credits. During the open enrollment period which ended on February 15th, there were 96,197 Kansans (including those who enrolled during the special enrollment period that ended on February 22nd) who selected a health insurance plan through the federal exchange, and 76,958 of them have been told they will receive premium tax credits to help pay for their plans during 2015. Whether or not they receive that financial assistance to purchase insurance depends on the outcome of this case.

Supporters of the Affordable Care Act (ACA) point out that if the Court determines that the IRS regulation is invalid, more than 7 million individuals in 34 states may no longer be eligible to receive tax credits to help pay for their health insurance premiums. The federal government and insurance industry officials have warned that the cost of health insurance for those individuals who are able to continue to pay their premiums without tax credits and remain in the health insurance market will rise significantly, resulting in even more individuals eventually losing coverage.

On the other hand, critics of the ACA point out that a Court ruling that the premium tax credits are not allowable in the 34 states that have not established their own exchanges, including Kansas, could save the U.S. Treasury an estimated $24 billion in subsidies that would otherwise be paid in 2015. This includes nearly $195,000,000 in insurance subsidies to people living in Kansas.

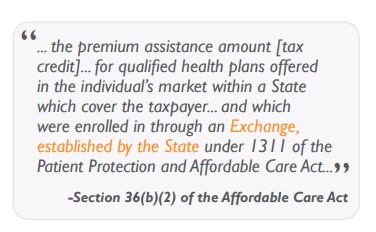

The plaintiffs in the King case, represented by attorney Michael Carvin, contend that the language in Section 36B of the Affordable Care Act, which describes the calculation of premium tax credits, only allows individuals enrolled in an “Exchange established by the State” to receive tax credits. Since Kansas and 33 other states have so far elected not to establish a state exchange, individuals in those states are enrolling in insurance plans purchased through the HealthCare.gov exchange website established and operated by the federal government.

The federal government, represented by Solicitor General Donald Verrilli, Jr., contends that while the ACA authorizes states to establish exchanges, it also authorizes the federal government, in Section 1321 of the ACA, to “establish and operate such Exchange within the State” if a state elects not to establish a state exchange. (Emphasis added). The federal government argues that Congress intended an “Exchange established by the State” to include exchanges established by the federal government and the availability of tax credits through those exchanges.

As expected, Supreme Court Justices Ginsberg, Breyer, Kagan and Sotomayor appear to be inclined to support the position of the federal government and the availability of tax credits in states using the federal exchange. Justices Alito, Scalia and Kennedy were active in challenging the position of the government, but Justice Kennedy was also active in raising questions for the plaintiffs. Chief Justice Roberts asked very few questions and Justice Thomas was silent throughout the arguments. Legal experts have suggested that Chief Justice Roberts and Justice Kennedy are potential votes for either side of the case.

Issues Raised During Argument

Standing

At the beginning of the plaintiffs’ argument, Justice Ginsberg raised the issue of standing. Under federal law, courts are limited by the Constitution to only hearing cases in which a plaintiff, the individual or party who has filed the claim, has actually suffered an injury. The four plaintiffs in this case, who reside in Virginia, have claimed they are liable to pay the individual mandate tax penalty for 2014 if tax credits are available in states, like Virginia, that chose not to establish a state exchange. Prior to last week’s arguments, questions had been raised as to whether any of the four plaintiffs will actually be required to pay the penalty. Although there was no definitive response to Justice Ginsberg’s questions from either Mr. Carvin or General Verrilli regarding whether any of the four plaintiffs actually had standing, neither of the lawyers seemed interested in having the case decided on this issue.