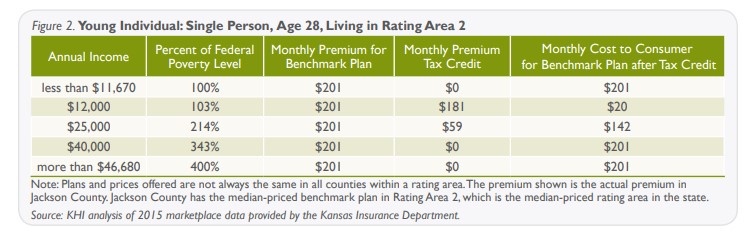

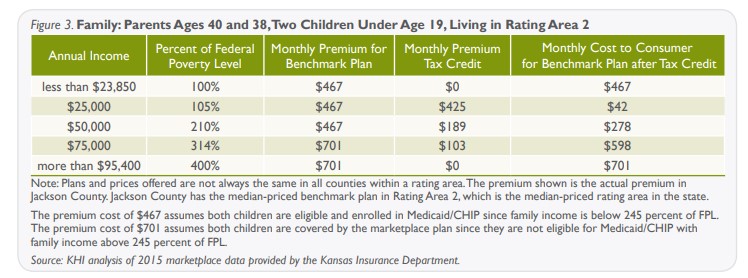

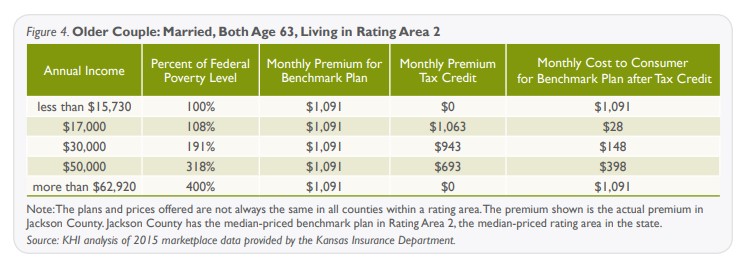

Some Kansans with incomes very near the poverty line have the option of paying as little as $20 per month for a silver plan after premium tax credits are applied.

These credits can be worth hundreds of dollars each month for these enrollees. People with higher incomes qualify for much smaller tax credits and could pay substantially more per month in premiums for the same plan.

Those with incomes between 100 and 250 percent of FPL also qualify for additional cost-sharing subsidies through the ACA if enrolled in a silver plan. These subsidies reduce out-of-pocket costs when healthcare services are utilized.

Rating Areas

Kansas is divided into seven “rating areas” for plan premiums based on regional factors such as previous health care spending and the cost of living. Plan premiums vary across rating areas. For example, the silver benchmark plan in the state’s most expensive rating area—the Northwest corner (area four)—is 17.5 percent more expensive on average than in the least expensive rating area—the South Central region (area six).

Medicaid “Eligibility Gap”

As originally written, the ACA called for all states to expand their Medicaid programs to cover all adults with incomes under 138 percent of FPL. Therefore, premium tax credits for people with incomes below the poverty level were not included in the law. However, the 2012 Supreme Court decision on the ACA made Medicaid expansion optional for states.

States electing not to expand coverage—such as Kansas— are faced with an “eligibility gap,” as people with incomes below 100 percent of FPL are not eligible for Medicaid, and they also cannot qualify for premium tax credits to buy private coverage through the marketplace. As a result, these individuals receive no assistance for their health insurance premiums, as illustrated in the first row of Figures 2-4. KHI estimated earlier this year that nearly 182,000 Kansans fell into the eligibility gap and 78,400 of those individuals were uninsured.

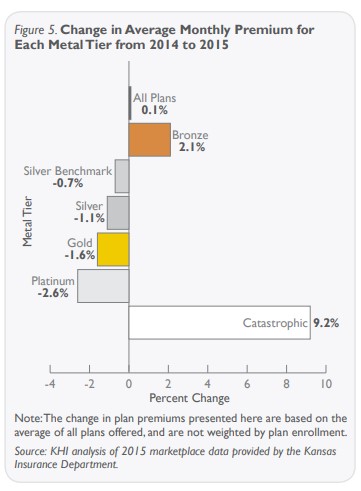

Comparing 2014 to 2015 Plan Premiums

Health insurance premiums tend to increase based on numerous factors including rising health care costs and increasing utilization. In addition, under the ACA, rates can increase for individuals based on their age.

On average, premiums for plans available in the marketplace changed very little between 2014 and 2015. The average premium across all plans increased just 0.1 percent. If catastrophic plans (which are available only to individuals under age 30 or those with a special hardship exemption) are excluded, the average premium decreased 1.1 percent across all plans.

For the silver benchmark plan, the average premium decreased by 0.7 percent. Average premium changes for all tiers are shown in Figure 5.