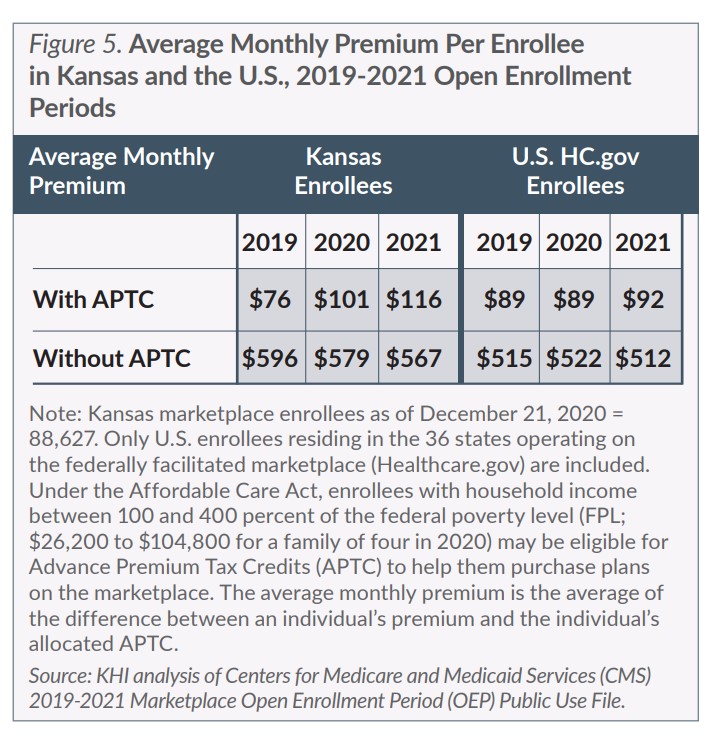

The average premium for Kansas enrollees without APTC was 4.9 times higher than for those receiving APTC ($567 compared to $116). Generally, Kansas enrollees paid monthly premiums that were 10 to 25 percent higher than the average monthly premium paid by enrollees across all 36 states (including Kansas) operating on the federally facilitated marketplace.

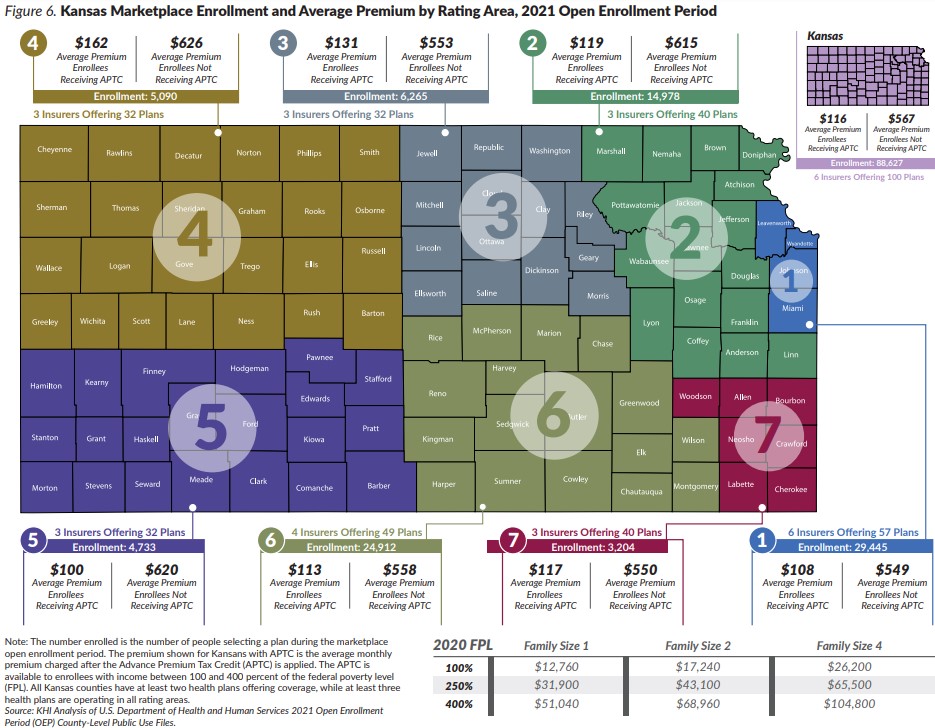

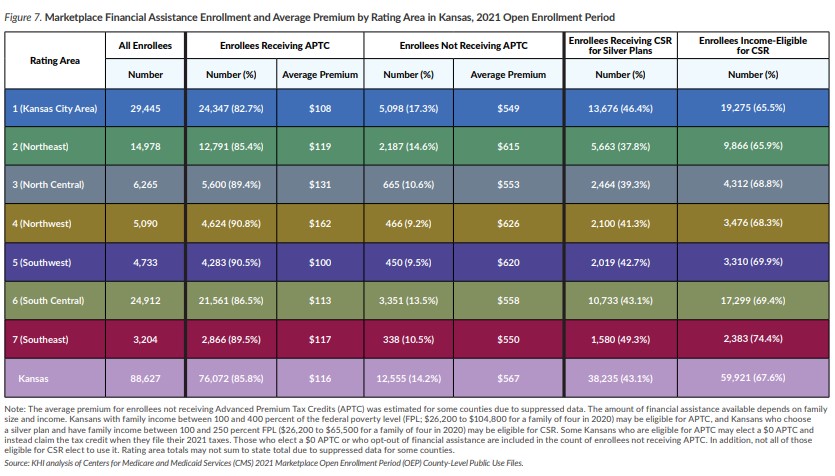

Figures 6 and 7 provide information on average monthly premiums in the seven rating areas across Kansas. Among those selecting a plan during the 2021 OEP and receiving APTC, enrollees living in Northwest Kansas had the highest average monthly premium of $162, which was 62.0 percent higher than enrollees living in Southwest Kansas and receiving APTC, who had the lowest average monthly premium of $100.

Stand-Alone Dental Insurance

For the 2021 plan year, there were 12 stand-alone dental policies offered by four insurers on the Kansas marketplace and 12,357 Kansans selected a standalone dental plan — a 5.0 percent decrease compared to 2020.

Looking Ahead

While enrollment in the Kansas marketplace had steadily declined since 2016, when 101,555 enrollees selected a plan, there was a slight uptick in enrollment for the 2021 OEP compared to 2020. Total enrollment in the 2021 plan year is expected to increase further due to the SEP which began on February 15, 2021, in response to the COVID-19 pandemic and runs through August 15, 2021. During this SEP, individuals who were not able to sign up for marketplace coverage during the previous open enrollment period that ended in December 2020 can enroll and current Kansas enrollees can reevaluate their coverage and enroll in a different plan. The SEP also is an opportunity for uninsured residents to enroll in coverage, as well as people who are covered under non-ACA-compliant plans, such as short-term plans, Farm Bureau plans, or health care sharing ministries.

On March 11, President Biden signed the American Rescue Plan Act of 2021 (ARP) into law, which includes provisions that expand access to and increases the dollar value of the premium tax credit in 2021 and 2022. The increased tax credit eliminates insurance premiums for households with income between 100-150 percent FPL. Additionally, households with income above 400 percent FPL that were previously not eligible for APTCs will now be eligible and will have their premiums capped at 8.5 percent of their income. However, APTC is still not available for people with family income below 100 percent FPL, leaving the so-called coverage gap in states that have not expanded Medicaid. Current enrollees will need to reapply for coverage to take advantage of the expanded tax credit provisions in the ARP.