Introduction

Lowering the cost of health care is consistently one of the top priorities for Americans. Prior to the COVID-19 pandemic, public opinion polls found that more than two-thirds of Americans, regardless of party affiliation, considered lowering the cost of health care to be very or extremely important. Health care spending is determined by the number of people served, the number of services provided and the amount paid per service.

While consumers are concerned about the cost of health care overall, the prices paid for hospital services across Kansas are the focus of this brief. Hospitals accounted for the largest share (37 percent) of the $3.2 trillion in national health care spending in 2019, and the largest share (39 percent) of the $22.2 billion spent in Kansas in 2014, the most recent estimate available.

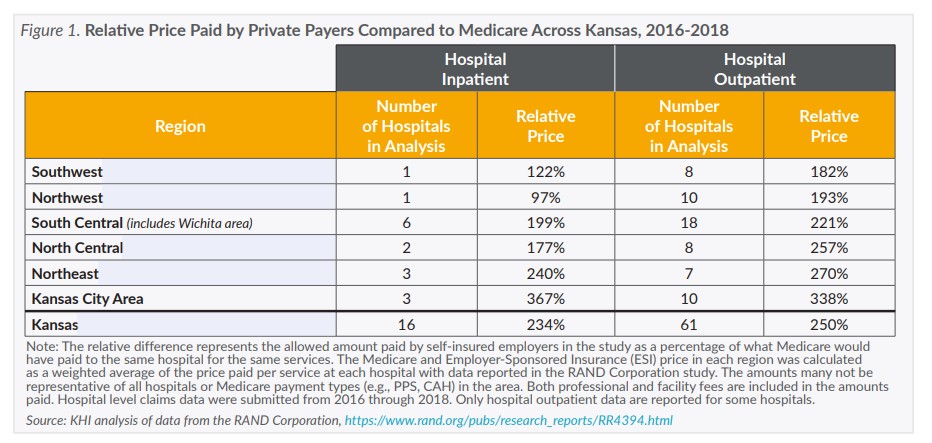

Using data from a recently released study by the RAND Corporation, this issue brief finds that hospital prices paid for hospital services by self-insured employers vary at least two- to three-fold in Kansas. Higher prices lead to higher health care spending, which is directly reflected in the out-of-pocket cost’s consumers pay and the increasing cost of health insurance premiums for employers and consumers.

The RAND study summarizes 2016 through 2018 claims submitted by community hospitals across the nation. The study includes claims submitted to self-insured employers from 49 states (including Kansas) and Washington, D.C., and additional claims submitted to private payers (e.g., insurance companies) as recorded in All Payer Claims Databases in six states (Connecticut, Colorado, Delaware, Maine, New Hampshire and Rhode Island). The study provides a first look at variations in hospital prices across Kansas and makes the case for a more comprehensive source of information on health care prices. A new federal funding opportunity discussed on page 4 could improve access and availability of claims data for understanding health care prices in Kansas.

How are Hospital Prices Set?

The price for hospital services would ideally use a systematic methodology that balances the cost to the provider of organizing and delivering services and the need of the payer to manage financial risk. However, the methods used by payers to establish prices are many and complex. The RAND study’s analytical approach was based on the Fee-For-Service (FFS) payment model. The FFS payment model sets a price for every individual health care item, service or bundle of services and in most cases providers are reimbursed at the set price regardless of the charged amount.

Pricing Services in Medicare

Medicare sets hospital prices in most cases using FFS formulas defined in federal statute and regulation. The pricing formulas vary by provider type and setting (e.g., hospital inpatient and outpatient departments), but there are common features among them. Each formula typically pays a base rate for an item, service or bundle that is adjusted to account for the complexity of the patient’s case, policy-based incentives (e.g., bonuses for meeting quality standards) and geographic factors like local wages or rurality. Because of these formulas there are minimal differences across individual providers in the prices paid for the same item or service in the same setting. In other words, hospitals within the same region should receive similar payments from Medicare for similar services. One notable exception relates to Critical Access Hospitals (CAHs), to which Medicare currently pays 101 percent of allowable costs in order to keep essential services in rural communities.

Pricing Services with ESI

Employer Sponsored Insurance (ESI) prices are determined through negotiations, and the contracts with providers are generally not available for public review. The negotiations likely consider factors including consultation with providers and outside experts, public data on quality, technology used, expected outcomes, geographic needs, efforts of network providers to consider social determinants of health, the cost of treatment and its effectiveness, the provider’s payer mix (e.g. the proportion of uninsured, Medicaid, Medicare and private insurance patients) and market power.

Market power is often cited as a significant factor in determining the prices paid for hospital services. Hospitals that are more in demand by patients are generally able to negotiate higher prices with payers, and conversely payers with a higher percentage of enrollees in a hospital’s service area generally can negotiate lower prices. There also is some limited evidence from one study in another state that insurance providers serving as third-party administrators may be willing to agree to higher prices for services provided to employees of self-insured employers because the third-party administrator bears less risk for these payments.

Why Do Hospital Prices Vary?

Despite the critical role of prices in overall spending, little is publicly known about why the prices that ESI pays vary or how those prices are determined. While this is beginning to change — as of January 1, 2021, hospitals are required by federal regulation to provide accessible pricing information online — some hospitals around the country are refusing to publish their prices or making them difficult to find, and court challenges are being launched. Even when prices are published online it is difficult for consumers to determine the quality or value, they are receiving for the prices paid and to understand more generally why prices vary among services and providers.

Differences in clinical quality and payer mix are often cited as a reason for price variation between hospitals. However, the RAND study found neither an association between ESI price and a hospital’s Medicare and Medicaid payer mix nor a strong correlation between price with either quality or patient safety. Although RAND standardized the prices paid at each hospital to make them comparable, they acknowledged that their methods may not have completely accounted for differences in payer mix and service intensity (e.g., the care coordination, type, number and frequency of providers required to meet patients’ needs) among hospitals.