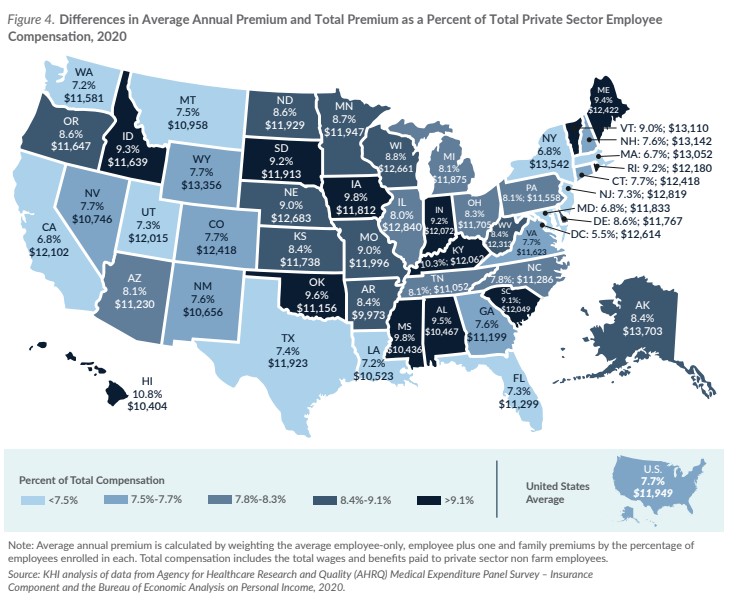

The average premium in Kansas is similar to the average premium in the United States. However, because compensation in Kansas is lower than compensation nationally, the percentage of compensation paid towards premiums is higher. In 2020, the total premium in Kansas was 8.4 percent of total compensation for private sector employees compared to 7.7 percent nationally.

There are also significant differences in the average annual premium for employer-sponsored health insurance across the country. The average annual premium varied from a low of $9,973 in Arkansas to a high of $13,703 in Alaska. Some of the variation in average premium is explained by differences in plan selections between states (e.g., 60.2 percent of employees in Arkansas were enrolled in employee-only coverage in 2020 compared to 53.9 percent in Kansas) and some is due to differences in premiums for employee-only, employee-plus-one and family plans. For example, in Arkansas the premium for a family plan is 15.6 percent lower than in Kansas, an employee-plus-one plan is 8.3 percent lower than in Kansas and an employee-only plan is 3.9 percent lower than in Kansas on average.

Discussion

The growth in health insurance premiums is mostly accounted for by the increase in healthcare spending. Actuaries from the Centers for Medicare and Medicaid Services (CMS) find that expenditures for private health insurance enrollees increased 40.4 percent nationally from $819.86 billion in 2010 to $1.15 trillion in 2020. Spending on healthcare services and goods accounted for 86.9 percent of private health insurance expenditures in 2020 and had increased 37.9 percent since 2010 from to $725.10 billion to $1.00 trillion.

As premiums rise, the financial burden on employees and employers increases. To mitigate this rising burden, employers may choose to reduce benefits in the plans they offer (e.g., increase cost sharing or deductibles, or implement narrower provider networks), increase their employees’ share of premiums, which ultimately could affect employee health, productivity and retention, or alter their business plans to accommodate higher compensation for their employees. To the extent that healthcare costs rise faster than their revenue, employers offering health insurance may have to decide between hiring and growing their business and increasing total compensation for their current employees.

Researchers have identified several factors that may explain differences in premiums for employer-sponsored insurance plans among states including employees’ health status, insurer competition, benefit design, prices for healthcare services, utilization, plan selection (e.g., family vs employee-only coverage), and other coverage options available in the state.

The data in this analysis do not identify the specific factors contributing to the differences in annual premiums between Kansas and other states, but there may be an opportunity for Kansas employers and policymakers to work together to determine if there are policy or legislative options that could impact the cost of employer-sponsored health insurance in the state.