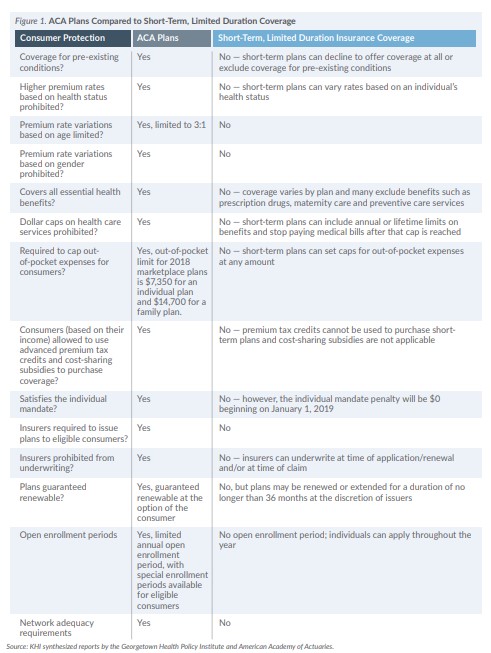

Introduction

On October 12, 2017, President Donald Trump issued an Executive Order promoting two types of health insurance coverage as alternatives to the health insurance plans available to individuals and small businesses under the Affordable Care Act (ACA) — association health plans (http://bit.ly/KHI-1810) and short-term, limited duration insurance (STLDI). The order directed the secretaries of the Treasury, Labor and Health and Human Services (the “Departments”) to consider expanding the availability of STLDI by allowing it to cover longer periods and be available for renewal by consumers. The president noted that since STLDI is not subject to the ACA’s mandates and regulations, it can be an affordable alternative to the health plans sold through the ACA marketplaces for individuals who do not obtain coverage through their employer.

In response to the president’s order, the Departments issued a proposed rule on February 21, 2018, stating the intent to “lengthen the maximum period of short-term, limited duration insurance, which will provide more affordable consumer choice for health coverage.” During the public comment period for the proposed rule, which ended on April 23, the Departments received more than 12,000 comments. The Final Rule, which lengthened the maximum period to three years, was released on August 1. It will become effective October 2, 2018.

Short-Term, Limited Duration Insurance (STLDI)

STLDI is a type of health insurance coverage originally designed to allow consumers to fill temporary gaps in coverage they might experience when transitioning from one health plan to another, for example, when changing jobs or relocating. Under the requirements applicable to individual health insurance coverage established under the Public Health Service Act (PHS Act), STLDI is not considered individual health insurance and is not subject to the market reforms and other requirements of the ACA.

Although the PHS Act does not define STLDI, up until 2016 federal regulations implementing the Health Insurance Portability and Accountability Act of 1996 (HIPAA) defined STLDI as “health insurance coverage provided pursuant to a contract with an issuer that has an expiration date specified in the contract … that is less than 12 months after the original effective date of the contract.” However, following the enactment of the ACA, some insurers began to offer STLDI coverage that lasted for just less than one year (364 days). To address concerns that STLDI was being sold to consumers as a type of primary health insurance coverage, as well as concerns about the impact of adverse selection on the risk pool for ACA-compliant plans, the Obama administration issued a final rule in October 2016 that changed the long-standing definition of STLDI to specify that it only could provide coverage for less than three months.