Per Capita Allotment for Medicaid

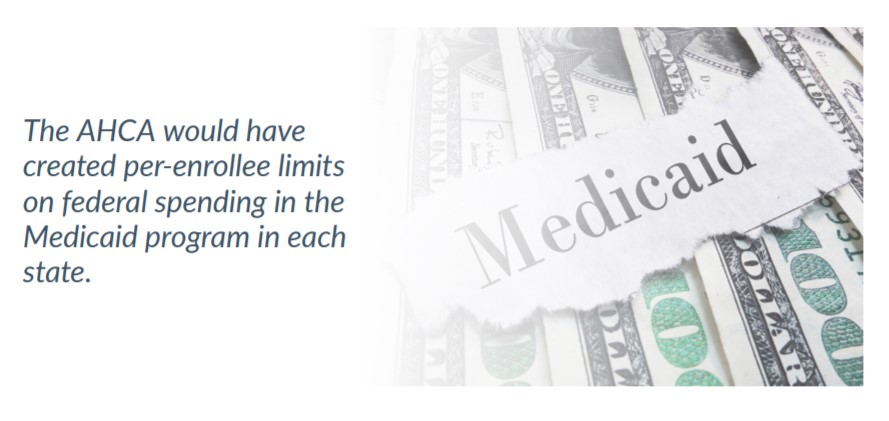

The AHCA proposed a substantial change to the way the Medicaid program would be financed. It would have created per-enrollee limits on federal spending in the Medicaid program in each state, based upon the state’s fiscal year (FY) 2016 expenditures for five populations—elderly, blind and disabled, children, non-expansion adults and expansion adults. A per-enrollee spending cap for each population in FY 2019 would have been set using the FY 2016 calculations, increased by an inflation rate. In subsequent years, each state’s targeted per-enrollee spending amount (or cap) would have grown by the increase in the medical care component of the consumer price index (urban) for all consumers. In FY 2020 and beyond, states spending more than the targeted per-enrollee amount for all the defined populations combined would have had their Medicaid funding reduced by the difference the following year.

The bill (as introduced on March 6) indicated the per capita cap for newly eligible adults in states that expanded Medicaid after FY 2016 would be based on a state’s per-enrollee spending on non-expansion adults in FY 2016. (As noted above, in the later manager’s amendment, the option to expand with enhanced federal support would have been removed for non-expansion states.)

Some expenses and populations would have been exempt from the caps, including Disproportionate Share Hospital (DSH) payments, administrative costs, individuals receiving assistance through an Indian Health Service provider, the breast and cervical cancer program, and so-called “partial benefit” enrollees, such as Medicare enrollees for whom Medicaid pays cost-sharing.

In response to feedback from some states, the manager’s amendment would have allowed states to opt to receive a block grant for traditional adult and child populations starting in FY 2020. Funding for the block grant would have been determined using the same base-year calculation as used for the per capita allotments.

New reporting requirements for data on expenditures within defined categories would have been created, and federal matching funding for improving data reporting systems would have increased temporarily. The U.S. Department of Health and Human Services (HHS) also would have been required to conduct audits of each state’s reported enrollment and expenditures for FY 2016 and FY 2019 (the years used to set the per capita caps) and subsequent years.

Safety Net Funding for Non-Expansion States

One way that the legislation proposed to address concerns of providers in non-expansion states was to allow states to make adjustments in the amounts paid to Medicaid providers. For calendar years 2018 through 2021, non-expansion states would have received an increased matching rate of 100 percent for these payment adjustments, and 95 percent in calendar year 2022. A state’s allotment from the total of $2 billion provided annually would have been calculated based on the number of individuals in the state with incomes below 138 percent of FPL in 2015. States that expanded Medicaid in 2018 or after would not have been eligible for the enhanced safety net funding after expansion.

Disproportionate Share Hospital (DSH) Cuts

Medicaid DSH payments, which are made to hospitals to offset losses on uninsured and Medicaid patients, were to be phased down to about half of their total under the ACA, with the assumption that providers would have less uncompensated care after ACA implementation. However, Congress has delayed the start of the cuts three times, paying for the delay by deepening the cuts scheduled for future years. The AHCA would have repealed DSH cuts scheduled for 2018 in states that did not expand Medicaid, and would have repealed DSH cuts in 2020 for states that had expanded Medicaid.

Other Medicaid Provisions

The bill would have rolled back several other key provisions of the ACA, including states’ expanded authority to make presumptive eligibility determinations for beneficiaries, other than for children, pregnant women and breast and cervical cancer patients. It also would have repealed a 6-percentage point bonus in the federal match rate for certain community-based attendant services and supports provided in a 1915(k) waiver, which Kansas does not have.

It also would have reverted the mandatory Medicaid income eligibility level for children back to 100 percent of FPL from 133 percent of FPL. States like Kansas that had used the Children’s Health Insurance Program (CHIP) to cover certain age groups of children above 100 percent of FPL were required by the ACA to expand Medicaid eligibility for children up to 133 percent of FPL. The U.S. Supreme Court opinion in the 2012 case NFIB v. Sebelius made Medicaid expansion for adults optional for states, but it did not reverse it for children.

In a significant change from current policy, the bill would have limited the effective date for retroactive coverage of Medicaid to the month in which the applicant applied, beginning October 1, 2017. Currently, retroactive medical coverage can extend to three months prior to the month of application.

The manager’s amendment would have given states the option to institute work requirements for Medicaid for nondisabled, nonelderly and nonpregnant adults. The amendment was modeled after the requirements and exemptions in the Temporary Assistance for Needy Families program under current law.

The AHCA would have required individuals to provide documentation of citizenship or lawful presence before obtaining Medicaid coverage.

The bill also presented Medicaid proposals that would reduce costs for the states and the federal government, including a change in how income is determined for lottery winners.

The AHCA would have required states to redetermine the eligibility of Medicaid expansion enrollees every six months. The bill also would have increased the civil monetary penalty HHS can levy against someone who intentionally defrauds the Medicaid program.

Prevention and Public Health

Beginning in fiscal year 2019, the AHCA would have repealed appropriations of more than $1 billion each year for the Prevention and Public Health Fund, which was established by the ACA to fund prevention, wellness and public health initiatives administered by HHS. However, the bill would have provided for $422 million in supplemental funding in 2017 for the Community Health Center Fund, which awards grants to federally qualified health centers that provide medical, dental, mental health and reproductive health services to medically underserved populations.

Conclusion

While the American Health Care Act proposed by House Republicans has so far failed to get a vote in the House of Representatives, the contents of the proposed bill provide some insight into the priorities of Republican leadership and President Trump for the future of health reform. The changes made and proposed during negotiations around the bill provide a preview of key issues for future debate.