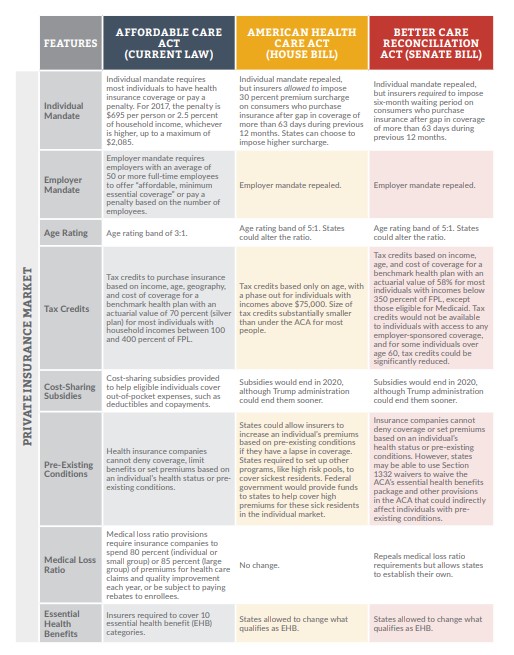

Repeals both the individual and employer mandates for insurance coverage.

Requires a six-month waiting period for individuals who experience a gap in coverage. Phases out enhanced federal funding for Medicaid expansion but proposes to address the “coverage gap” by allowing more low-income people to use tax credits to pay for premiums.

Makes premium subsidies unavailable to individuals who have access to any employer sponsored insurance and less generous for some who remain eligible and ends cost-sharing subsidies after two years.

States may be able to use Section 1332 waivers to waive the ACA’s essential health benefits package and other provisions in the ACA that could indirectly affect individuals with pre-existing conditions.

Phases out enhanced federal funding for Medicaid expansion, but proposes to address the “coverage gap” by allowing more low-income people to use tax credits to pay for premiums

Fundamentally changes how Medicaid is financed by creating hard caps on federal funding.

Introduction

After the Republican-controlled U.S. House of Representatives passed the American HealthCare Act (AHCA or House bill) by a margin of 217 to 213 on May 4, 2017, the bill moved to the U.S. Senate for approval. Almost immediately after the House vote, several Republican senators announced they did not support the AHCA—the bill designed to repeal and replace the Affordable Care Act (ACA)—and stated the Senate would be amending the House bill or drafting its own bill rather than voting on the AHCA as it passed the House.

After weeks of closed-door negotiations among select Senate Republicans, a “discussion” draft bill, the Better Care Reconciliation Act (BCRA or Senate bill) was released on June 22, 2017. Senate Majority Leader Mitch McConnell stated he would be calling for a vote on the bill—officially described as an amendment to the AHCA and adopting many of its provisions—in less than a week.

When the Congressional Budget Office(CBO) released its cost estimate report for the BCRA a mere four days later, it projected that 22 million more Americans would be uninsured by 2026 under the Senate bill, bringing the estimated total of uninsured Americans to 49 million by 2026, compared to a total of 28 million under current law. The CBO report also estimated that the Senate bill would reduce the federal deficit by $321billion over 10 years, primarily from savings due to ending the enhanced federal funding for the ACA’s Medicaid expansion, reduced premium tax credits, and reductions in projected future federal funding for state Medicaid programs. The House bill had been estimated to result in23 million more uninsured Americans by 2026and a $119 billion reduction to the federal deficit. Senator McConnell decided to postpone a vote on the BCRA until after the Senate’s Fourth of July week recess.

Like the AHCA, the Senate bill modifies a number of provisions in the ACA related to the private health insurance market and Medicaid, including ending the ACA’s enhanced funding for Medicaid expansion by 2024, but making tax credits for purchasing plans on the marketplace available to low-income people who don’t otherwise qualify for Medicaid. It would also, like the AHCA, place hard caps on future Medicaid spending growth by converting open-ended federal financing toper capita caps or block grants.

Private Insurance Market

Individual and Employer Mandates

Like the AHCA, the Senate bill would retroactively repeal to January 2016, both the individual mandate (which requires that most individuals purchase health insurance or pay a tax penalty) and the employer mandate (which requires employers with 50 or more full-time employees to provide “minimum essential coverage” health insurance for their employees or be subject to a tax penalty).

Coverage Incentive to Stabilize Individual Health Insurance Markets

With the repeal of the individual mandate, a planned amendment to the BCRA would require health insurers offering plans in the individual market to impose a six-month waiting period on individuals who had a gap in creditable coverage of more than 63 days in the 12 months prior to enrolling in current coverage. For individuals who qualify to obtain coverage during an open enrollment period (OEP) or special enrollment period (SEP), but are subject to the waiting period, coverage would begin six months after the date the individual submits an application for coverage. For individuals who submit an application outside of the OEP, do not qualify for an SEP, and are subject to the waiting period, coverage would begin the later of either (1) six months after the day on which their application was submitted, or (2) the first day of the following plan year.

Age Rating

Like the House bill, the BCRA would repeal the 3:1 age rating band (meaning premiums for older adults cannot be more than three times the amount of premiums for younger adults) required under the ACA and establish a 5:1 age rating band effective for 2019. States would have the option to implement a ratio that differs from the 5:1 ratio.

Tax Credits

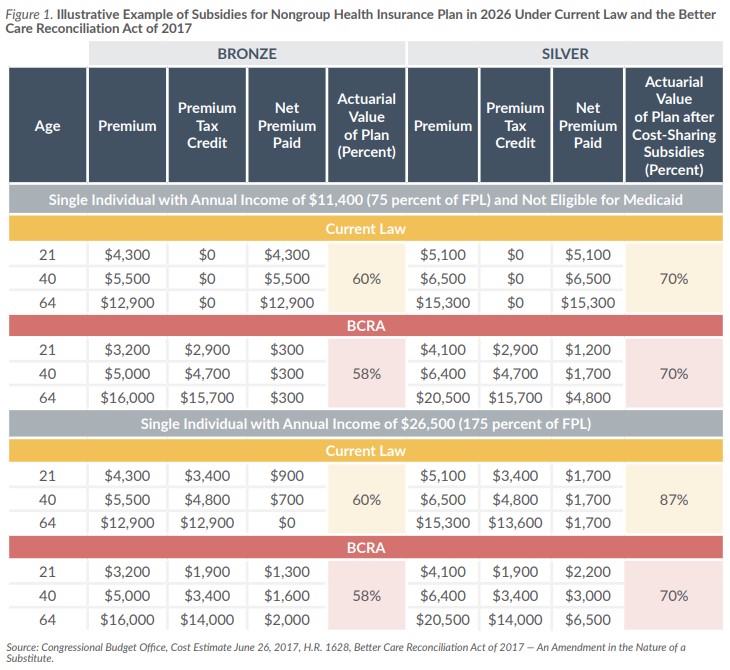

The BCRA would modify the income eligibility criteria for the ACA premium tax credits starting in 2020, when it would extend eligibility to individuals with incomes below 350 percent of the federal poverty level (FPL) who are not otherwise eligible for Medicaid. The bill would also restrict eligibility for the credits to “qualified aliens,” which would exclude individuals in the U.S. on worker or student visas, and would make individuals who are offered any employer-sponsored health plan, regardless of affordability or minimum value, ineligible for credits.

The determination of the amount of the BCRA tax credits would no longer be tied to the cost of the ACA’s second-lowest-cost silver plan (with an actuarial value of 70 percent) but would be based on the median premium of all qualified health plans with an actuarial value of 58 percent, just below the current actuarial value of an ACA bronze plan.

The formula for calculating the amount (based on percent of household income) that individuals and families would be required to contribute to the cost of their premiums would be based on age and income level. Percentages would range from 2.0 percent for those in the lowest income band, regardless of age, to 16.2 percent for those in the highest income band and the oldest age band. In general, individuals with incomes above 150 percent of FPL and over age 29 would be required to contribute more than younger or poorer individuals.

Cost-Sharing Subsidies

The BCRA would appropriate to the Secretary of the U.S. Department of Health and Human Services (HHS) the dollars needed to continue the cost-sharing subsidy program in the ACA—which reduces out-of-pocket costs for deductibles, copayments and coinsurance for marketplace health plan enrollees with incomes between 100–250 percent of FPL—from the date the bill is enacted until December 31, 2019, when the subsidies would be repealed. Health insurers have been lobbying the Trump administration to provide assurances of the continuation of the subsidies as they consider whether to participate in the ACA marketplaces across in the country in 2018.

Medical Loss Ratios

The ACA imposes medical loss ratio (MLR) requirements on health insurers that limit the portion of premium dollars they are allowed to spend on administration, marketing and profits. Under the law, insurers are required to spend at least 80 percent of their premium income from individual and small group health plans on health care claims and quality improvement. The MLR threshold for large group plans is 85 percent. Insurers who fail to meet the MLR requirements must pay rebates to consumers. The BCRA would sunset these MLR requirements beginning in 2019 and would allow states to set their own MLRs and required rebates for individual and group coverage.

Section 1332 Waivers for State Innovation

Section 1332 waivers were created by the ACA to allow states to pursue alternative strategies for increasing access to coverage, reducing premiums and increasing enrollment for their citizens, while retaining the basic protections of the ACA. States could waive or opt out of a number of ACA requirements, including certification of qualified health plans, requirements for essential health benefits, or the delivery of benefits through the marketplace, and could receive “pass through” funding equal to what premium taxes, cost-sharing subsidies, or small business tax credits would have been for the state’s citizens without a waiver. Under the ACA, the innovation strategies proposed and implemented by states are required to provide access to care that is at least as comprehensive and affordable as would be provided without the waiver and have no impact on the federal budget.

Although Section 1332 waivers became available to states at the beginning of 2017, there was limited interest among states, in part because of how the Obama administration interpreted budget neutrality and other requirements.

The BCRA does not modify the basic provisions of Section 1332 but would modify and expand the waiver option by amending the criteria required for waiver approval. States would no longer be required to demonstrate that their waiver plans would meet the comprehensive coverage, affordability and budget neutrality requirements established by the ACA. Instead, the bill would require HHS to approve a state’s waiver application unless it determined the state’s plan would increase the federal deficit.

The BCRA also would modify the portion of Section 1332 related to pass through funding to allow states to request that all, or a portion of, the aggregate pass through funding be paid directly to the state, although funding for cost-sharing subsidies and small business health insurance tax credits, which are available as pass through funding under the ACA, would be eliminated elsewhere in the bill in 2020. The BCRA would allow states to use funds appropriated for the Long-Term State Stability and Innovation Program created by the bill, as long as the planned use for the funds is consistent with the requirements for the use of funds under that program and would also appropriate $2 billion to HHS to provide grants to states for submitting a waiver application and implementing the state plan approved under the waiver until the end of federal fiscal year (FFY) 2019.

The waivers would be approved for up to eight years, or less if requested by the state, and could not be canceled by HHS once granted. They could be renewed in unlimited eight-year periods.

States that may have contemplated combined Section 1332 and 1115 waivers—for private insurance and Medicaid, respectively—but were not able to because of the way the Obama administration interpreted budget neutrality, might now have reason to consider them again, although the legislation does not explicitly define a process for combined waivers.

Taxes

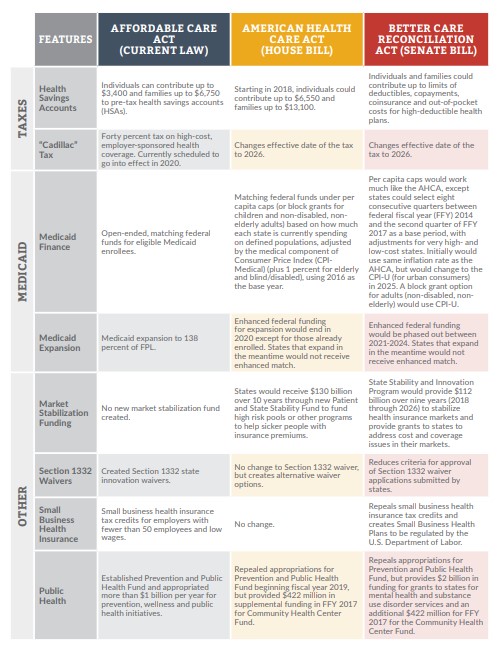

Like the House bill, the BCRA would repeal or modify several taxes or tax limitations imposed by the ACA, including the “Cadillac tax” on benefit-rich, employer sponsored health plans, and the cap on contributions to health savings accounts, and would establish different effective dates for some of the tax items.

State Stability and Innovation Program

The BCRA would establish the State Stability and Innovation Program and appropriate $112 billion over nine years to the Administrator of the Centers for Medicare and Medicaid Services (CMS) to be used to “address coverage and access disruption and provide support for states.” For 2018 through 2021, $60 billion of the funds would be provided to health insurance companies to stabilize premiums and encourage insurers to offer plans in the individual market. The remaining dollars would be used to create a Long-Term State Stability and Innovation Program that would provide funds directly to states for 2019 through 2026 to:

Provide financial assistance to high-risk individuals (projected to have high health care utilization) enrolling in the individual market who do not have access to employer-sponsored insurance;

Provide payments to health care providers; and,

Provide assistance to low-income individuals with private insurance coverage to reduce their outof-pocket costs (co-payments, coinsurance and deductibles).

Medicaid

The Senate bill, like the House version, would limit the federal government’s share of the cost of Medicaid by placing hard limits on the cost growth of the program. The per-person costs for most Medicaid enrollees would be limited to a base period’s costs increased by an inflation rate, known as a per capita cap. States also would have the option of using a block grant for nondisabled, non-elderly adults.

Repeal of Medicaid Expansion

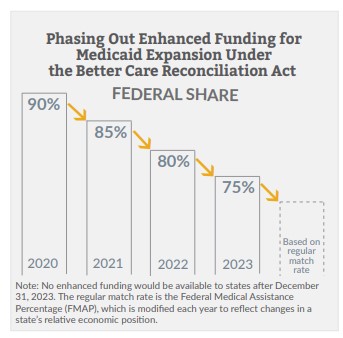

The BCRA includes a phase-out of the ACA’s enhanced federal funding for Medicaid expansion. Instead of ending it in calendar year 2020 as the House bill does, the Senate bill would phase out the enhanced expansion match rate starting in 2021. The enhanced rate would not be available at all after 2023. Like the House bill, the Senate bill would not provide for any enhanced match rate for states that expand Medicaid on or after March 2017.

Per Capita Allotment for Medicaid

The per capita cap would work much like the House version, with some modifications. Two changes are worth noting. First, the per capita caps on each eligibility group—seniors, people with disabilities, children and other adults—could be adjusted by up to 2 percent to penalize states with much higher-than-average costs, and to reward states with much lower-than-average costs. In addition, states would be allowed to select any eight-quarter period between FFY 2014 and the third quarter of FFY 2017 as the base period for setting the caps.

Like in the House bill, the inflation rate used to set the caps beginning in FFY 2020 would be the medical component of the Consumer Price Index, CPI-Medical, for children and some adults, and an additional 1 percent for seniors and those with disabilities. But in FFY 2025, the BCRA would start using the overall CPI for urban consumers, CPI-U, which is typically significantly lower than the CPIMedical.

In federal fiscal years 2023–2026, states that did not exceed their per capita caps would be eligible for quality-based bonus payments for Medicaid and the Children’s Health Insurance Program (CHIP). The total bonuses would be capped at $8 billion over the four years for all eligible states.

Flexible Block Grant Option

States could elect to accept a block grant for a five-year period for non-disabled, non-elderly adult enrollees, and with it waive a number of standard Medicaid requirements. The block grant would be adjusted annually by the CPI-U. States could keep any block grant funds not spent on enrollees and could use them for other health programs, or even non-health programs (with limitations that would be written in regulation by HHS). States would have a “maintenance of effort” requirement equivalent to the match rate for CHIP multiplied by the block grant amount (in Kansas, the post-ACA CHIP match rate is likely to be around 70 percent).

Safety Net Funding

From FFY 2018 to 2022, non-expansion states would share $2 billion in annual federal safety net funding for provider payment adjustments. The funds would be distributed based on the relative number of people in each state with incomes below 138 percent of FPL in 2015.

Disproportionate Share Hospital Payments

Non-expansion states would see the scheduled reductions in Disproportionate Share Hospital (DSH) payments canceled. Some non-expansion states with lower-than-average per-person DSH allotments would get a bonus to pull them up to the average.

Other Medicaid Provisions

As in the House bill, states would be permitted to implement work requirements for non-disabled, nonelderly, non-pregnant adults. The Senate bill would provide for a 5-percent bump in the federal match for administrative expenses related to implementing the work requirement.

The BCRA would phase down taxes on providers and health plans that are used to support Medicaid rates to a 5-percent cap. The current cap is 6 percent, and the bill would start lowering the cap by 0.2 percent per year in FFY 2021, finally landing on the 5-percent cap in FFY 2025. The Kansas Legislature this year raised the privilege fee (a form of provider tax) on health maintenance organizations, including the KanCare health plans, to 5.77 percent to generate funds to reverse the Medicaid reimbursement rate cuts.

States with managed care waivers that have been renewed at least once would no longer need to use the waiver renewal process, instead submitting a state plan amendment to continue waiver authority in perpetuity. Such “grandfathered” waivers could be modified only by a waiver amendment, but HHS would have just 90 days to review and approve an amendment or request more information (similar to the current state plan amendment process).

The BCRA would allow states to provide Medicaid coverage for qualified inpatient psychiatric hospital services for up to 30 consecutive days, and 90 days per year, to beneficiaries age 22–64. Current law prohibits use of federal funds for such services except at small facilities with no more than 16 beds or for limited, short-term stays for managed care enrollees. This modification to the so-called Institutions for Mental Diseases (IMD) Exclusion could open the door for larger crisis centers across the state.

Prohibition on Use of Federal Funds

The BCRA would prohibit state use of federal funding for defined “prohibited entities” for one year, whether directly or through managed care. The definition, which references family planning, abortion services, and total Medicaid funding in FFY 2014, appears to apply to Planned Parenthood. The prohibition would be in effect regardless of the established programmatic rules in Medicaid regarding choice of provider and non-exclusion of providers based solely on the range of services they provide.

Prevention and Public Health

Like the House bill, the BCRA would repeal all Prevention and Public Health Fund appropriations beginning in FFY 2019. However, as a response to the national opioid epidemic, $2 billion would be appropriated to HHS for FFY 2018 to provide grants to states to support substance use disorder treatment and recovery support services for individuals with mental illnesses or substance use disorders. The additional $422 million in funding for the Community Health Center Fund provided in the House bill is also included in the BCRA.

Conclusion

While it is uncertain whether the Better Care Reconciliation Act will be passed by the full Senate in the near future, or how it may be amended, it is clear that House and Senate Republicans continue to share a vision to repeal and replace the Affordable Care Act. Although Senate Republicans had hoped to vote on the bill prior to the Fourth of July week recess, it now appears they have much more work to do to get to consensus. A vote is now not expected until later this summer

About Kansas Health Institute

The Kansas Health Institute supports effective policymaking through nonpartisan research, education and engagement. KHI believes evidence-based information, objective analysis and civil dialogue enable policy leaders to be champions for a healthier Kansas. Established in 1995 with a multiyear grant from the Kansas Health Foundation, KHI is a nonprofit, nonpartisan educational organization based in Topeka.