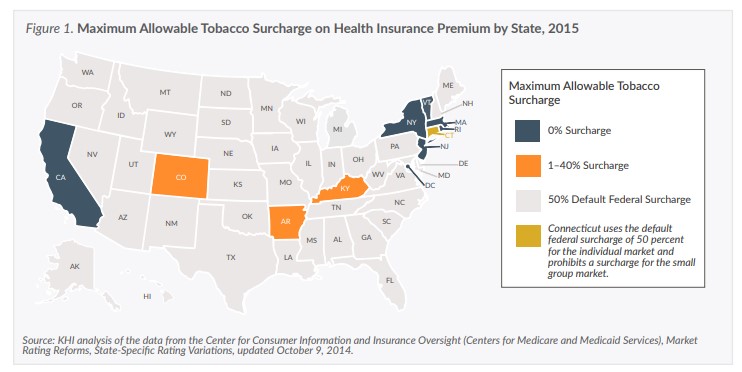

Maximum Allowable Tobacco Surcharge on Health Insurance Premium by State, 2015

States Vary on Higher Premiums Paid by Tobacco Users Under the ACA

Kansas insurers applying up to 44 percent surcharge for tobacco users in 2015

Key Points

-

- In January 2014, under the ACA, insurers were no longer permitted to consider health status and pre-existing conditions when calculating health insurance premiums. They were permitted to consider age, location and tobacco use.

- The federal rules state the calculation of the tax credit is based on the cost of the health plan before the application of the tobacco surcharge.

- Consumers are required to self-report if they are a tobacco user to the insurance companies. Surcharges may be waived if the consumer participates in a smoking cessation program.

- Consumer advocates fear the surcharge will deter tobacco users from purchasing health insurance.

Introduction

Under the Affordable Care Act (ACA), insurance companies are allowed to charge individuals who use tobacco products higher premiums for health insurance than non-tobacco users. This additional cost is added to premiums for tobacco users in the form of a tobacco use surcharge. Kansas Health Institute (KHI) staff reached out to representatives from health insurance companies offering coverage on the Kansas marketplace, national insurance industry officials and health policy experts to find out how this part of the ACA has been implemented and how it impacts Kansas consumers.

Prior to the enactment of the ACA, health insurance companies in Kansas, as in most states, considered the health status and history of individuals applying for insurance—including their use of tobacco products—when quoting premium rates. Under the ACA, for health plans issued on or after January 1, 2014, insurers are no longer permitted to consider health status or pre-existing health conditions when calculating premiums, but may only consider an individual’s age, geographic location and use of tobacco products. The surcharge was necessary to address the generally accepted premise that individuals who use tobacco products—regardless of their age—utilize more health care services than those who do not, and the higher costs associated with their health care should be borne by those who use these products. However, the federal regulation that dictates how the tobacco surcharge is to be administered does not necessarily ensure that all enrollees who use tobacco products are paying the required surcharge. It also limits the actions that can be taken by insurers to enforce payment of the surcharge.

The Creation of the Surcharge

During the development of the ACA, the federal drafters of the law advised insurance industry officials that they wanted to move to “community rating” for health insurance premiums, which requires insurers to offer health insurance policies within a given market at the same price to all persons, regardless of their current health status or health history. Industry officials instead proposed the use of “adjusted (or modified) community rating,” which would still prohibit insurers from using health status or health history to set premiums but would allow them to vary rates based on other factors such as age, gender and tobacco use.

The drafters were adamantly opposed to the use of gender in setting premiums but agreed to the use of age and tobacco when the industry argued that in the absence of these rating factors, all consumers would be paying more in premiums to account for the higher claims costs associated with older individuals and tobacco users. Industry representatives felt strongly it was a matter of fairness and personal responsibility that individuals who choose to use tobacco products should pay more for their coverage. Although the industry had charged as much as five times the base premium for tobacco users prior to the enactment of the ACA, the drafters and actuaries (acting on behalf of the industry) ultimately agreed to a much lower 50 percent increase in the premium, based on projections of the number of tobacco users likely to enroll for coverage beginning in 2014.

Although the primary purpose of the tobacco use surcharge was to respond to the insurance industry’s concerns regarding the higher cost of health care services for tobacco users, some members of Congress wanted to encourage insurers to work on getting consumers enrolled in smoking cessation programs.

Tobacco Use Surcharge Rules

Under the ACA, insurers are allowed to increase premiums up to a maximum of 50 percent for enrollees who use tobacco. Federal regulations define “tobacco use” as the use of tobacco products four or more times per week (on average) within the last six months. When applying for health insurance, consumers are asked to self-report whether they meet the “tobacco use” definition and their premium rate is calculated based on their response. If it is later determined that an enrollee failed to report their tobacco use, the insurer may retroactively apply the surcharge to the enrollee’s premium as if the information had been accurate from the beginning of the plan.

Prior to the ACA, an enrollee’s failure to disclose accurate information on their application for health insurance was just cause for rescission of their coverage—meaning the insurer could refuse to pay for claims and be refunded for any claims paid all the way back to the beginning of the enrollee’s policy. The ACA prohibits insurers from rescinding coverage for consumers who fail to report their tobacco use.

Insurers offering health plans to small employers (50 or fewer employees) may also impose the surcharge on employees who use tobacco products, but only in connection with a wellness program that allows the employees to avoid paying the higher premium if they agree to participate in a tobacco cessation program. Employees who fail to report their tobacco use are also subject to the same retroactive application of the surcharge.

Although the federal law allows states to limit the surcharge to less than 50 percent, or to adopt a narrower definition of tobacco use, most states, including Kansas, have defaulted to the federal rules. However, six states and the District of Columbia prohibit insurers from charging any surcharge on tobacco users, and three additional states limit the surcharge to less than 40 percent (Figure 1).

For the 2015 plan year, insurers offering coverage through the Kansas marketplace are applying surcharges ranging from zero to 44 percent. As allowed by the federal rules, the surcharge is higher for older enrollees in Kansas who smoke than for younger ones.

Surcharge Implementation

Under the rules established by the U.S. Department of Health and Human Services (HHS), consumers enrolling in coverage through the marketplace are required to self-report if they meet the definition of a tobacco user. Under this process, insurers are forced to trust the attestation provided by enrollees. In cases where insurers in the small group market waive the surcharge if an individual agrees to participate in a smoking cessation program, they must trust that the individual actually participates in the program.

With this self-reporting system, insurers are very concerned that tobacco use is being under-reported since there is no incentive for enrollees to accurately disclose their use. Some very large, national insurers attempt to scan enrollee claims data to look for high-cost claims that may be related to tobacco use or try to determine whether enrollees are actually using their smoking cessation benefits. However, this type of claim history review, and review of enrollee medical records, is very labor intensive and costly. With the limits on administrative costs imposed under the ACA’s medical loss ratio rules, which allow insurers to use only 15 percent of premium dollars for all administrative expenses, this practice is largely cost-prohibitive for most insurers.

Since HHS regulations do not permit insurers to rescind coverage for individuals who have failed to report their tobacco use or failed to participate in a smoking cessation program, insurers are limited to adjusting enrollees’ premiums or encouraging them to use their smoking cessation benefits. Although insurers are permitted to retroactively adjust an enrollee’s premiums, the collection of that additional premium is another administrative burden.

When calculating the surcharge percentages that will be applied, insurance company actuaries attempt to project the number of tobacco users, by age, who are likely to enroll in their plans. One Kansas insurance company reported that, surprisingly, the number of actual tobacco use enrollees came within 5 percent of their estimate.

Kansas marketplace insurers generally rely on enrollee attestations for purposes of applying the surcharge and, unlike some large, national companies, are not actively reviewing enrollee claims to identify tobacco users who failed to report their use. One insurer stated it was doing some basic monitoring, but that it was not closely watched. All Kansas marketplace insurers agreed that reviewing claims and medical records was cost-prohibitive and not a good use of their time and resources. However, they also stated that if tobacco use is discovered, they do adjust enrollees’ premiums to collect the surcharge or attempt to encourage them to utilize the smoking cessation benefits provided under their health plan.

Opposition to Tobacco Surcharge

Since HHS announced its rules for implementation of the tobacco use surcharge in early 2013, some consumer advocates, such as the American Lung Association, along with some national health policy experts, have expressed concerns about the surcharge as an impediment to purchasing coverage, particularly for low-income tobacco users. Advocates acknowledge that in the absence of the tobacco surcharge, insurers would likely spread the costs of tobacco-related illnesses across their entire risk pool population, thereby increasing premiums for all enrollees. However, they worry that the higher premium rates for tobacco users will result in some individuals going without coverage because it is unaffordable.

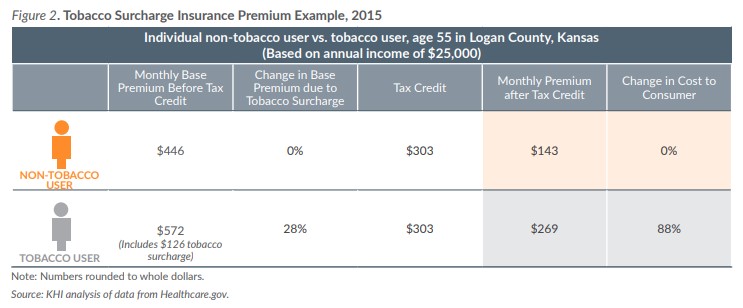

Under the federal rules for calculation of advance premium tax credits to help consumers purchase insurance, the calculation of the tax credit is based on the cost of the health plan before the application of the tobacco surcharge. Therefore, the enrollee pays the full amount of the surcharge that is added to the premium after the application of the tax credit (Figure 2). Under the tax provisions of the ACA, if an individual’s health insurance premium, including any tobacco surcharge, exceeds 8.05 percent of their household income, they are not subject to the individual mandate penalty for failing to have health insurance. However, their exemption from the tax penalty still leaves them without insurance coverage for needed health care services or to access smoking cessation benefits.

Advocates and health policy experts also have pointed out that there is no evidence or data suggesting that the imposition of the tobacco surcharge discourages the use of tobacco products. It does not appear the ACA drafters agreed to the surcharge during their discussions with the insurance industry based on a belief that the surcharge would act as a deterrent to the use of tobacco products. However, the requirement in the small group market that insurers waive the surcharge for individuals who agree to participate in a smoking cessation program, and the inclusion of smoking cessation benefits as a part of the ACA’s required essential health benefits, do suggest that some members of Congress were interested in encouraging individuals to stop using tobacco products.

Conclusion

The ACA provision allowing insurers to apply a maximum surcharge of 50 percent to collect additional premiums from tobacco users was Congress’ response to the health insurance industry’s concerns about the higher health care claims costs for tobacco users of all ages. However, the federal regulation associated with the implementation of the surcharge does not guarantee that all tobacco users will pay the surcharge, and places significant limitations on insurers attempting to enforce the application and collection of the surcharge.

While Congress, the insurance industry and health advocates all agree that the surcharge is intended to ensure that non-tobacco users will not be forced to bear the burden of higher claims’ costs for tobacco users, advocates and health policy experts are concerned that the surcharge makes coverage unaffordable for tobacco users, particularly those with low incomes.

In response to these concerns, some states have limited the maximum surcharge insurers can apply to less than 50 percent, and others have prohibited the use of any surcharge for tobacco users. Nonetheless, the majority of states including Kansas have allowed insurers doing business in their states to assess the maximum surcharge of 50 percent.

About Kansas Health Institute

The Kansas Health Institute supports effective policymaking through nonpartisan research, education and engagement. KHI believes evidence-based information, objective analysis and civil dialogue enable policy leaders to be champions for a healthier Kansas. Established in 1995 with a multiyear grant from the Kansas Health Foundation, KHI is a nonprofit, nonpartisan educational organization based in Topeka.