The state contributed the difference for members contributing less than $1,100 annually (or approximately $92/month).

Additional cost-sharing was applied to emergency room (ER) visits for conditions that did not require emergency treatment. These less urgent emergency room visits had a $25 copay for non-caretakers and a $3 copay for caretakers. Total cost-sharing was limited to 5 percent of annual household income, which is the existing traditional Medicaid limit.

Benefits and incentives

In addition to the POWER accounts, each member received $500 worth of preventive care services, smoking cessation services and mammograms.

HIP covered services including pharmaceuticals, laboratory tests, inpatient and outpatient services and mental health treatment. Maternity care, dental and vision were not covered for adults. Maternity services continued to be covered by Hoosier Healthwise, the state’s traditional Medicaid program. Members who received recommended preventive services could have their remaining POWER account balance rolled over into the next calendar year, while those who did not lost their remaining balance.

Notable exclusions or limitations

HIP had a $300,000 annual and $1,000,000 lifetime coverage limit for any member’s health care costs. In addition, if members failed to pay into their POWER account regularly (with a two-month grace period), they were removed from the HIP program and prevented from re-enrolling for 12 months.

Cost and enrollment

HIP enrollment was capped to limit the cost to the state. The program averaged 40,721 members monthly between January 2008 and December 2012. Of that number, 36,500 were adults without children participating in HIP.

At times, 50,000 additional Indiana residents were waiting to enroll.

Between 2008 and 2012, Indiana was about $1 billion under the budget neutrality requirement of its waiver. The state’s share of the cost of HIP largely was financed through a cigarette tax.

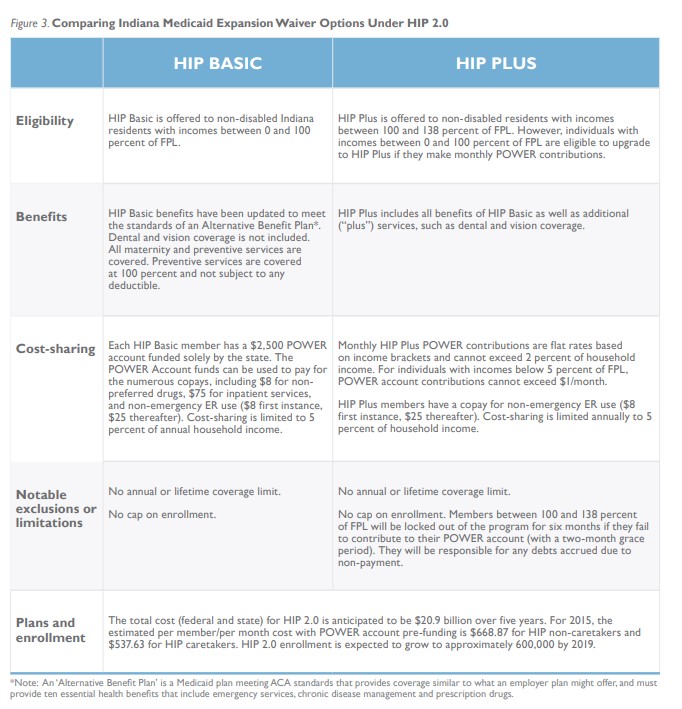

Indiana’s HIP 2.0

Medicaid expansion plan (February 1, 2015–present)

With the availability of 100 percent federal funding until 2017 for Medicaid expansion under the ACA, Indiana proposed an updated version of its Healthy Indiana Plan. HIP 2.0 moves all low-income, non-disabled adults from traditional Medicaid into two private programs, HIP Basic and HIP Plus, as shown in Figure 3. These programs have different coverage and cost-sharing requirements.