However, in its June 2012 ruling on the ACA, the U.S. Supreme Court made Medicaid expansion essentially optional for states.

As of January 2014, Kansas and 24 other states have not expanded Medicaid, creating a gap between existing Medicaid eligibility and eligibility for premium tax credit assistance.

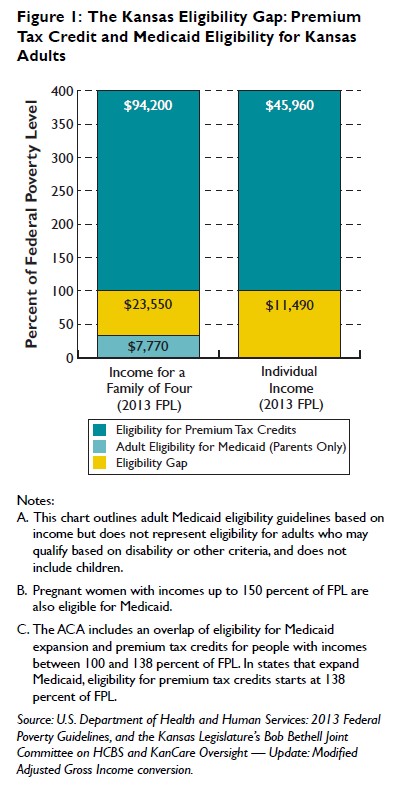

In Kansas, the existing Medicaid eligibility level for non-elderly adults is among the lowest in the country. For parents and guardians, income must be less than 33 percent of FPL, or about $7,770 annual income for a family of four. And in most cases, childless adults who are not disabled or elderly cannot qualify for Medicaid in Kansas regardless of how poor they are, as shown in Figure 1 .

Who Falls into the Eligibility Gap?

In Kansas, adults with annual incomes below the FPL — $23,550 for a family of four and $11,490 for an individual — are not eligible for premium tax credits when purchasing insurance through the marketplace. Childless adults (regardless of income) and parents with incomes above 33 percent of FPL also do not qualify for Medicaid. The lack of access to premium tax credits, while also not being eligible for Medicaid, creates what is called the eligibility gap. There is no eligibility gap for children because Kansans age 18 and younger in families with annual income up to 245 percent of FPL are eligible for Medicaid or CHIP. Kansans age 65 and older are eligible for insurance through Medicare. Therefore, all Kansans in the eligibility gap are age 19–64.

While Kansans in the eligibility gap are exempt from the ACA’s penalties for not obtaining health insurance, they continue to be financially responsible for the health care they need.

How Many People Fall into the Eligibility Gap?

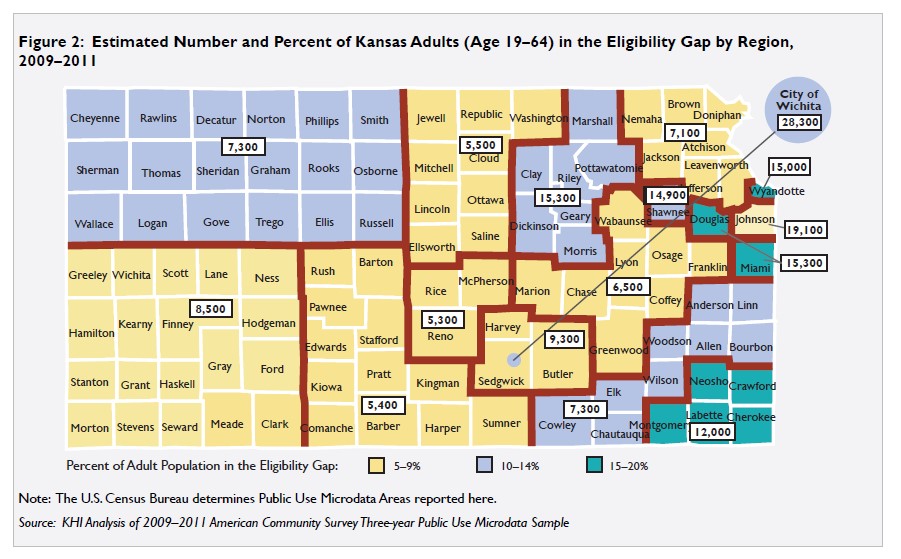

Nearly 182,000 Kansans fall into the eligibility gap. Figure 2 shows the number and percent of non-elderly Kansas adults in the eligibility gap across the state. The City of Wichita has the highest number of adults, 28,300 — 13 percent of the city’s adult population — in the eligibility gap.