Introduction

Now that President Obama has been reelected for a second term, implementation of the Affordable Care Act (ACA) seems likely to continue, though widespread opposition remains. Critics claim that the law is poorly designed and won’t come close to achieving its goals; supporters insist that the health care system is doomed to fail without the major overhaul.

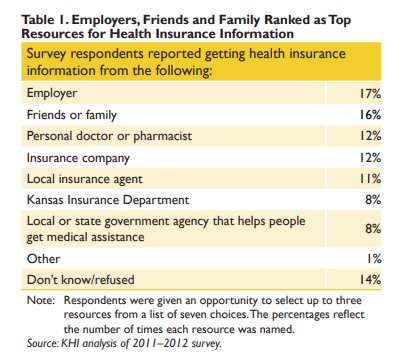

As Kansas policymakers contemplate the next steps for health reform in the state, it is important to include the perspectives of everyday Kansans in the planning. To better understand Kansans’ thoughts on our health care system, the Kansas Health Institute was commissioned by the Kansas Insurance Department to conduct a telephone and online survey and a series of focus groups between November 2011 and January 2012. This brief, the first of two, summarizes what Kansans had to say about the current state of health care and the improvements they would like to see. The second brief, available at www.khi.org, illustrates Kansans’ knowledge of the ACA and examines the health reform resources they find most trustworthy.

Most Kansans Satisfied with Private Insurance

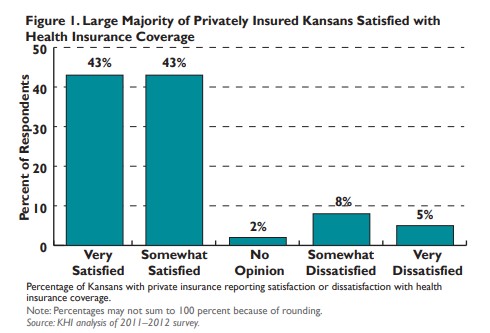

Nearly one out of every five Kansas adults is uninsured. Those with private health insurance, however, seem generally happy with their coverage. KHI surveyed 834 Kansans between the ages of 18 and 64, and a large majority — 86 percent — of those with private health insurance indicated that overall they were very or somewhat satisfied with their coverage. This was true of people who receive health insurance from an employer or union as well as those who purchase coverage directly from an insurance company (such as an individual policy from Blue Cross Blue Shield). As shown in Figure 1, only 13 percent of Kansans with private health insurance were somewhat or very dissatisfied with their coverage.