Insurance Marketplace Now Open—Plan and Cost Options for Kansans

9 Min Read

Oct 01, 2013

By

Robert F. St. Peter, M.D.,

LeAnn Bell, Pharm.D.

Key Points

While technical challenges may initially limit the online functionality, the Kansas marketplace features four insurance companies offering 72 plans at four coverage levels, or “tiers,” in addition to low-cost catastrophic plans.

In each Kansas county, at least two companies sell insurance through the marketplace and the average number of plans available is 37. The national average is 53 plans.

Many low- and moderate-income Kansans will receive assistance purchasing insurance through premium tax credits.

The average monthly premium for the “benchmark” insurance plan — a middle-of-the-road plan in terms of covered benefits and cost — in the Kansas marketplace is $260, below the national average of $328 and lower than all but four other states.

Kansas and other states that have not expanded Medicaid as allowed under the health reform law created an unexpected “coverage gap” where people with incomes below the federal poverty level may not be eligible for Medicaid nor financial assistance in the marketplace

Introduction

After more than three years of preparation and debate, the health insurance marketplace created by the Affordable Care Act (ACA) opened this week in Kansas for enrollment in coverage starting as early as Jan. 1, 2014. The Kansas marketplace is run by the federal government, as are the marketplaces in 25 other states. In the remaining states, 17 are managing their own marketplaces and seven are partnering with the federal government. While the initial rollout is likely to experience technical challenges and limited online functionality, the plans available and the prices for coverage in the marketplace are described in this brief.

Health insurance marketplaces allow individuals and small businesses to compare and buy health insurance. The marketplaces were included in the ACA to increase access to health insurance, which most U.S. citizens will be required to have starting in 2014. Private insurance companies offer the health insurance plans, which must cover a standard set of benefits that include common health services. No one seeking insurance can be denied coverage or charged more due to health status or pre-existing conditions. The cost of coverage is based on the number and age of those covered, where they live, smoking status and the level of cost-sharing desired. For most people with limited income, the federal government will provide financial assistance to buy insurance in the marketplace.

Individuals and employers in Kansas will continue to be able to buy insurance outside the marketplace and, with some limitations, can choose to keep the same insurance they now have. The number of Kansans who choose to purchase their insurance through the marketplace will depend on how appealing they find the plans and the prices offered.

Does the Kansas Marketplace Offer a Good Selection of Plans?

The Kansas marketplace includes 72 plans sold by four companies: Blue Cross Blue Shield of Kansas, Blue Cross Blue Shield of Kansas City, Coventry Health Care of Kansas and Coventry Health and Life Insurance.

Plans sold on the marketplace are arranged in four coverage tiers — bronze, silver, gold and platinum — plus “catastrophic” plans that are available only to people who are under age 30 or meet specific criteria. All plans cover roughly the same services, but the tiers differ based on cost-sharing features. Consumers who purchase a bronze tier plan will pay, on average, lower premiums for the insurance but a higher share of the deductibles, co-pays and co-insurance for health care. Consumers who purchase a platinum tier plan will pay more in premiums but a lower share of the cost of health care they receive.

Gold and silver plans have monthly premiums and cost sharing requirements that fall between those for bronze and platinum plans. Catastrophic plans are low-cost, high-deductible plans that require the enrollee to meet a substantial deductible before providing benefits, with the exception of providing many free preventive care services required by the ACA.

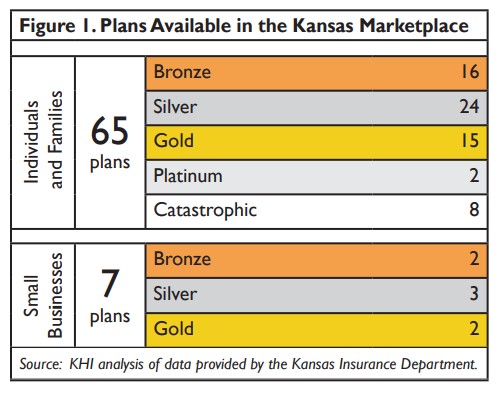

Of the 72 plans, 65 are offered to individuals and families and seven are offered to small businesses. Each insurer offers a variety of plans to individuals and families, spread across the coverage tiers. For individuals, two plans are platinum tier, 15 are gold, 24 are silver, 16 are bronze and eight are catastrophic coverage plans. For small businesses, two plans are gold tier, three are silver and two are bronze, as shown in Figure 1.

The plans and their cost vary across the state by so-called “rating areas” based on factors including previous health care spending and the cost of doing business in each area. While not all insurers offer the same plans across Kansas, every county has at least two companies selling insurance through the marketplace. The average number of plans offered to families and individuals in each county is 37, below the national average of 53 plans, according to recent data from the U.S. Department of Health and Human Services (HHS). This has caused some to question whether the choice of plans will be sufficient to attract consumers to the marketplace in Kansas.

Are Plans Affordable in the Kansas Marketplace?

HHS reports that the average monthly premium for the “benchmark” insurance plan — a middle-of-the-road plan in terms of covered benefits and cost — in the Kansas marketplace is $260, below the national average of $328, and lower than all but four other states. Understanding the price of insurance coverage in the Kansas marketplace gets complicated quickly. First, there is the total monthly premium that will be paid to the insurance company. Then, there is the part of the premium paid by the person being covered. The two can be very different because through the ACA, low- and moderate-income people can receive financial assistance to pay their health insurance premiums.

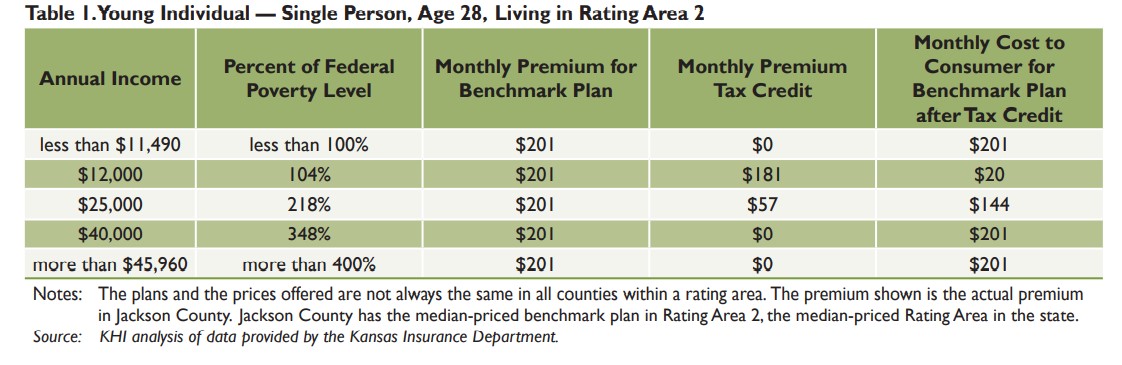

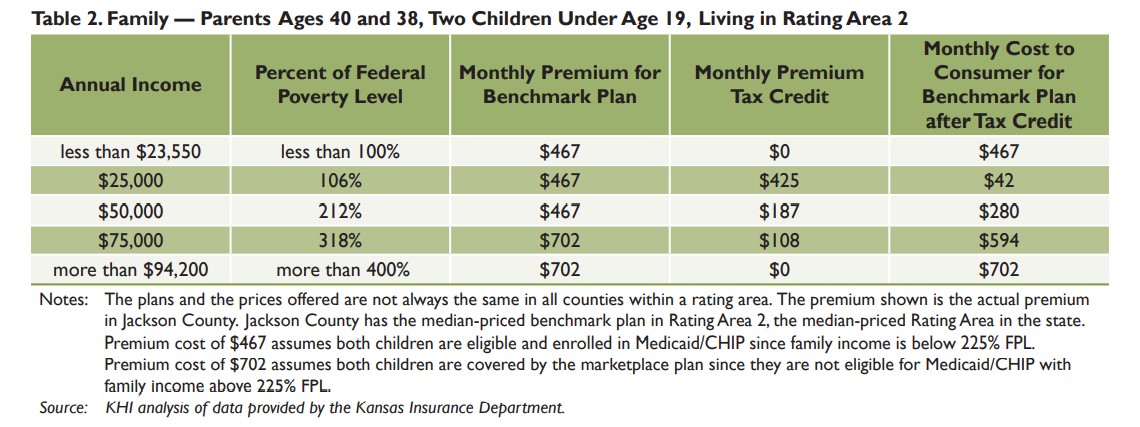

There are seven rating areas in Kansas. Several plans are offered in each county, including a benchmark plan, which technically is the second-lowest-cost silver plan in each county. The cost of insurance coverage will vary based on the ages and number of people being covered, where they live, whether they smoke and the level of cost-sharing selected. Here’s one example: For a family of four, with 40- and 38-year-old parents and two children, total monthly premiums for the benchmark plan across the state range from $651 to $771, an 18 percent difference between the most and least expensive rating areas. The monthly premiums for the same benchmark plan for a 28-year-old individual range from $186 to $221, a 19 percent difference, as shown on the map insert.

Premium Tax Credits Available for Those with Low and Moderate Incomes

Families and individuals with incomes between 100 and 400 percent of the federal poverty level (FPL) will be able to use premium tax credits to help purchase insurance in the marketplace. The consumer will pay the difference between the total monthly premium and the premium tax credit. To encourage participation in the marketplace, premium tax credits cannot be used to purchase insurance outside the marketplace.

For example, assistance will be available to individuals with annual income between $11,490 (100 percent of FPL) and $45,960 (400 percent of FPL) and families of four with annual income between $23,550 (100 percent of FPL) and $94,200 (400 percent of FPL). The amount of assistance is based on income and is designed so that people with incomes at 100 percent of FPL pay no more than 2 percent of their income toward the premium for the benchmark plan, while people with incomes between 300 and 400 percent of FPL pay no more than 9.5 percent.

The federal government pays the premium tax credit directly to the insurance company to reduce the upfront cost for the enrollee. The amount paid to the insurer on behalf of the enrollee is reconciled at the end of each year with the individual or family income on the tax return. Tables 1 and 2 provide examples of how the tax credits affect the cost of insurance premiums for families and individuals in Kansas.

The Coverage Gap — An Unexpected Situation

As originally written, the ACA called for the expansion of Medicaid eligibility to people with incomes below 138 percent of FPL (annual income of $15,856 for an individual and $21,404 for a couple). Premium tax credits for people with incomes below the poverty level were, therefore, not included in the law. However, in June 2012, the Supreme Court ruled that Medicaid expansion under the ACA was optional for states. In states that have not expanded Medicaid eligibility, including Kansas, this creates an unexpected situation where people with incomes below the federal poverty level may not be eligible for Medicaid nor cost-sharing assistance in the marketplace — creating the so-called “coverage gap.” These individuals will not be subject to the individual mandate penalty for not having insurance.

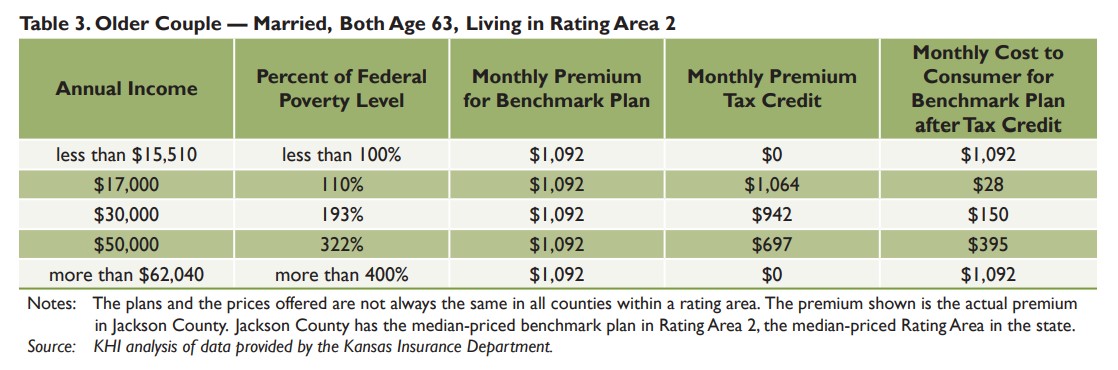

For example, a 63 year-old husband and wife with annual income of $15,000 (97 percent of FPL) would not receive assistance to buy insurance in the marketplace, therefore their cost for coverage would be $1,092 per month. They also would not be eligible for Medicaid in Kansas. However, the same couple with slightly higher income of $17,000 (110 percent of FPL) would pay only $28 toward their insurance premium each month because they qualify for a tax credit of $1,064, as shown in Table 3. This paradox, where people with incomes below the poverty level are not offered a benefit available to those better off, likely will generate discussion in states that have chosen not to expand Medicaid.

Other Tiers of Coverage

Although premium tax credits are based on the benchmark plan, consumers are able to enroll in another coverage tier if they determine it will better fit their health care needs. If they qualify for a premium tax credit, that credit can be applied to any plan in any coverage tier: bronze, silver, gold or platinum. However, tax credits may not be used to purchase catastrophic plans.

Looking Forward

The next year will be a critical time for health insurance marketplaces across the country. Their success depends on the decisions of consumers, businesses and insurers. Consumers will now have the choice to use the marketplace — or not — depending on how well it works and what is offered. Businesses — both those that currently offer insurance and those that do not — will decide whether to purchase insurance for their employees in the marketplace. Insurers will use this first year to determine whether their plan prices are too high, too low, or just right and how to make the marketplace profitable. A key question in those states that did not expand Medicaid in 2014 is what, if anything, will be done to address the coverage gap that exists for those who are too poor to qualify for premium tax credits in the marketplace, but aren’t eligible for Medicaid.

Access additional publications in the Documents & Downloads section.

About Kansas Health Institute

The Kansas Health Institute supports effective policymaking through nonpartisan research, education and engagement. KHI believes evidence-based information, objective analysis and civil dialogue enable policy leaders to be champions for a healthier Kansas. Established in 1995 with a multiyear grant from the Kansas Health Foundation, KHI is a nonprofit, nonpartisan educational organization based in Topeka.