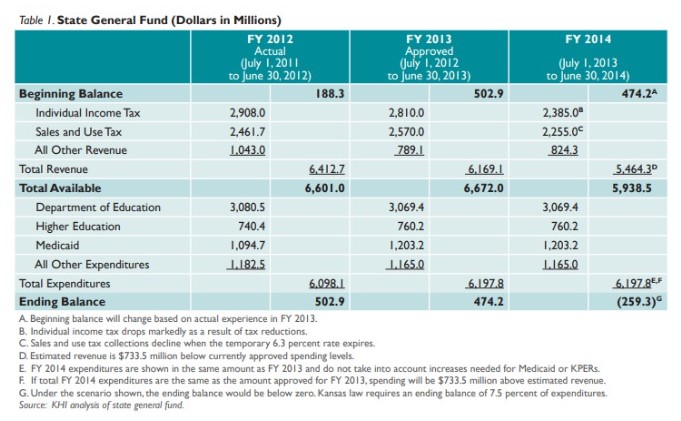

The FY 2012 column shows the actual experience with revenue collections and expenditures in the most recently completed fiscal year. The next column shows the approved budget for FY 2013 — the fiscal year that will be half-completed when the Legislature begins meeting in January 2013.

The FY 2013 approved budget begins with a bank balance of $502 million. Revenue and expenditures almost balance. In FY 2013 individual income tax receipts begin to go down as income tax cuts adopted by the 2012 Legislature take effect. Spending from FY 2012 to FY 2013 for education remains flat, but Medicaid expenditures go up to accommodate higher enrollments and replace temporary federal funding made available to states during the recession. Total approved spending in FY 2013 is up about $100 million from FY 2012.

FY 2014 starts with an expected bank balance of $474 million, although that number may grow or diminish depending on what actually happens during the remainder of FY 2013. The revenue numbers reflect the consensus revenue estimate completed in November 2012. Expenditures for FY 2014 are assumed to be the same as in FY 2013. The FY 2014 column shows that with total resources available of $5.939 billion, spending the same amount as in FY 2013 leads to a $259 million negative balance. That result does not meet the Kansas law that requires the budget to have an ending balance of at least 7.5 percent of expenditures. For a budget with expenditures of $6.197 billion, the ending balance law requires a minimum balance of $465 million.

FY 2014 Revenue

Receipts drop markedly in FY 2014 for two principal reasons: the expiration of a temporary sales tax and dramatic income tax reductions enacted for 2013.

Sales and use taxes are currently based on a 6.3 percent rate that temporarily was increased from 5.3 percent in FY 2011 to counteract revenue declines caused by the recent recession. On July 1, 2013, the rate will decrease to 5.7 percent, with 0.4 percent newly dedicated to the state’s highway fund. If FY 2014 sales and use tax receipts continued to be based on a 6.3 percent rate, SGF collections would be about $425 million higher.

Revenue decline from steep individual income tax reductions began in FY 2013, with the full effect realized in FY 2014. Previous top income tax rates go from 6.45 percent and 6.25 percent to 4.9 percent, while the lower income tax rate of 3.5 percent drops to 3.0 percent. In addition, the incomes of many business owners become completely exempt from state income tax.

FY 2014 Expenditures

Pressure to increase spending comes largely from the areas of school finance, Medicaid and payments for public employee retirement benefits.

State payments to public schools constitute half of current SGF spending and have climbed in recent years to replace temporary federal stimulus funds. However, the base amount of state aid per pupil has declined from a high of $4,400 in FY 2009 to $3,838 in FY 2013. An active lawsuit filed by a number of school districts seeks additional state support for public education.

The state portion of Medicaid currently consumes almost 20 percent of the SGF budget. Although Kansas Medicaid is being converted to a full managed care system called KanCare, that conversion is only predicted to slow expenditure growth rather than reduce overall Medicaid expenses.

Finally, the state has struggled to make the Kansas Public Employees Retirement System more financially sound by increasing the state contribution each year. Despite implementing a redesigned retirement system for current and future employees, the state must add approximately $50 million to the budget to cover the required state contribution for FY 2014.

Key Decisions Ahead

The revenue estimated for FY 2014 falls $733 million below current spending. Raising revenue, cutting expenses or doing both constitutes the most direct way to deal with the imbalance. However, the difference is so substantial that simply leaving the temporary 6.3 percent sales tax rate in place or making small cuts to programs would not close the gap. Balancing revenue and expenditures only through reduced spending would require a 12 percent across-the-board cut.

Alternatively, the state could ignore the ending balance law and spend down all or a portion of the available bank balance as a way to get through FY 2014. However, that short-term solution does not solve the imbalance between receipts and expenditures. Other alternatives include cutting spending in what remains of FY 2013 to lower the expenditure base and transferring money from other funds to the SGF.

No matter what solutions lawmakers choose, the FY 2014 budget presents many challenges that could have a direct effect on health programs and other key services.

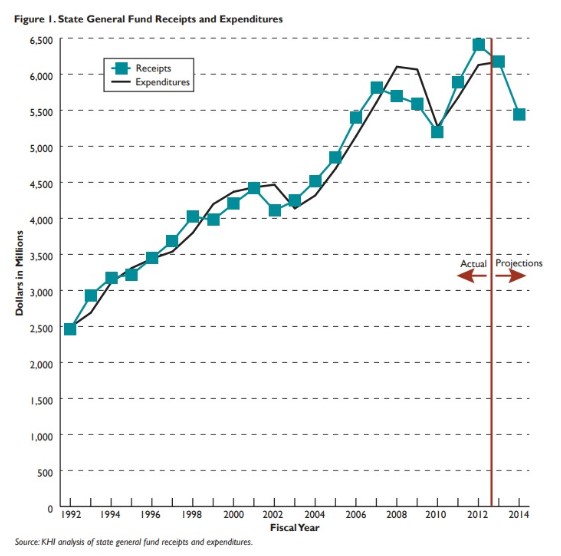

State General Fund History

Figure 1 depicts a history of State General Fund receipts and expenditures and shows the expected steep drop in FY 2014 revenue.