Insurance Exchange Will Provide Many Kansas Consumers With New Options

7 Min Read

Jan 08, 2013

By

LeAnn Bell, Pharm.D.

Key Points

More than 500,000 Kansans may have some reason to consider using the health insurance exchange to purchase coverage, though some are more likely to use it than others.

About 1.7 million Kansans are likely to continue with the coverage they have now.

The exchange will provide small employers and their workers with more options.

The exchange will serve as a gateway for determining eligibility for federal tax credits as well as Medicaid and the Children’s Health Insurance Program (CHIP).

Introduction

It’s well known that the Affordable Care Act — the controversial federal health reform law — requires virtually all U.S. citizens to obtain health insurance starting in 2014. Kansas and several other states challenged the so-called individual mandate but the U.S. Supreme Court ruled it constitutional.

To help people more easily obtain coverage, the ACA requires new online marketplaces called health insurance exchanges to be operational in every state by the time the mandate takes effect in 2014.

When it comes to setting up the exchanges, states have three options.

They can design and operate their own, adhering to federal guidelines.

They can partner with the federal government.

They can default to the federal government.

The Brownback administration did not support attempts by Insurance Commissioner Sandy Praeger to implement a state-based exchange. It also opposed her subsequent efforts to partner with the federal government on an exchange. As a result, the federal government will likely design and operate the Kansas exchange.

When consumers use the exchange they will find out whether they are eligible for federal tax credits to help them pay for private coverage. It will also operate as a gateway for determining eligibility for Medicaid and the Children’s Health Insurance Program (CHIP).

Who Will Use the Exchange?

Any Kansan can purchase coverage through the exchange starting in 2014. But some are more likely to use it. Uninsured Kansans are among the most likely to use the exchange as are those who now purchase coverage directly from insurance companies in the individual market and those who get coverage through small employers — those with fewer than 50 employees.

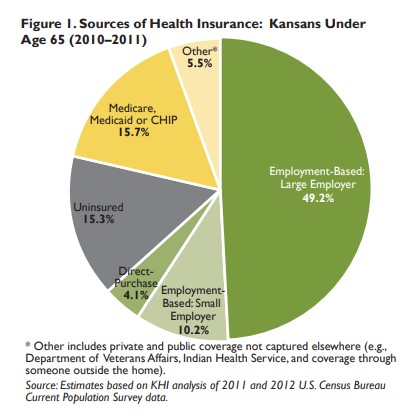

Figure 1 shows where the 2.4 million Kansans under age 65 get their insurance today. Almost three-fourths of them — about 1.7 million — are expected to keep their current coverage. These include Kansans who get coverage through employers with 50 or more workers.

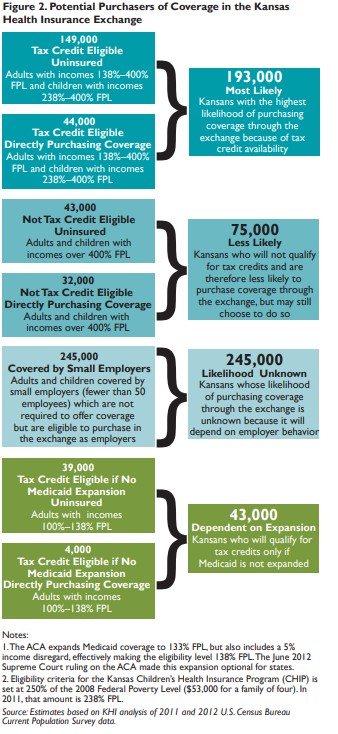

Large numbers of low-to-moderate income Kansans who qualify for federal tax credits are expected to use the exchange to purchase coverage. There are approximately 149,000 uninsured Kansans in this category — those with incomes starting at 138 percent of FPL, and up to 400 percent of FPL. For a family of four, that would be about $31,800 at the low end and $92,200 at the high end. In addition, an estimated 44,000 Kansans who currently directly purchase policies in the individual market would be eligible for tax credits, which may allow them to purchase less expensive coverage in the exchange. As shown in Figure 2, these two groups account for the 193,000 Kansans most likely to use the exchange.

There are about 43,000 uninsured Kansans who earn too much to be eligible for federal tax credits. However, because of the individual mandate many of these individuals may also end up purchasing coverage through the exchange. The same is true for the 32,000 Kansans who are not eligible for tax credits and are currently directly purchasing coverage in the individual market.

The biggest questions surround the approximately 245,000 Kansans who are covered through small employers — both private and public — that the ACA does not require to offer coverage because they employ fewer than 50 workers. These employers have several options. They can continue to purchase private group coverage outside of the exchange, obtain group coverage through the exchange or allow their workers to purchase individual policies in the exchange. Predicting what they will do is difficult. Some analysts expect that many of them will at least consider dropping their plans and sending their employees to purchase individual coverage in the exchange. Others predict there will be little to no change in the number of persons with employment-based coverage in the small-group market, or even a small increase.

The ACA initially allows each state to determine which employers can purchase coverage in the exchange. They can restrict that option to employers with fewer than 50 workers or extend it to those with fewer than 100. Our estimates assume that Kansas will initially allow only employers with fewer than 50 workers to do so.

About 101,000 of the Kansans who are covered through small employers would be eligible for federal tax credits if their employers dropped coverage and allowed them to purchase individual policies in the exchange.

Medicaid Expansion and the Exchange

The Supreme Court decision upholding the ACA struck down specific language in the law that authorized federal officials to withhold Medicaid funding from states that decline to expand eligibility for the program. That makes estimating the impact of the Medicaid expansion on the exchange difficult. The Brownback administration has not yet decided whether Kansas will participate in the expansion, which, if implemented, would make 315,000 low-income Kansans eligible for the program.

Currently, Kansas’ Medicaid eligibility for adults is among the lowest in the country at less than 32 percent of FPL — $5,900 for a family of four. And only caregiver adults such as parents and guardians are eligible at that level. Childless adults who are not disabled cannot qualify for Medicaid today regardless of how poor they are. The expansion would make all adults earning less than 138 percent of FPL — $30,660 for a family of four — eligible for the program.

If Kansas does not expand Medicaid, the ACA allows tax credits to be provided to individuals starting at 100 percent of FPL — $23,050 for a family of four. Approximately 43,000 Kansans with incomes between 100 percent and 138 percent of FPL would be eligible for tax credits to purchase coverage in the exchange if Medicaid is not expanded. This group includes 39,000 uninsured Kansans and 4,000 Kansans who today directly purchase coverage in the individual market.

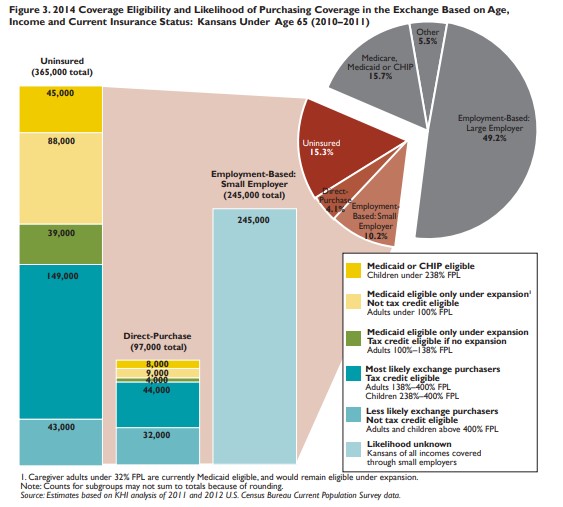

A decision to not expand Medicaid would also leave 88,000 uninsured adults ineligible for the program and also ineligible for tax credits. The implications of policy decisions about the Kansas health insurance exchange and Medicaid expansion are complex, as shown in Figure 3.

Many Will Remain Uninsured

Experts agree that even with full implementation of the ACA, some Kansans will remain uninsured. A 2011 analysis by nonprofit Urban Institute indicated that as many as 167,000 Kansans could remain uninsured — roughly 7.1 percent of the state’s population. Currently about 365,000 Kansans under age 65 — about 15 percent — are uninsured.

The Urban Institute analysis shows that almost half of 15 percent would be undocumented immigrants who those who would continue to lack coverage would be because of their status would not be eligible either for eligible for but not enrolled in Medicaid. An additional Medicaid or to purchase coverage in the exchange.

About Kansas Health Institute

The Kansas Health Institute supports effective policymaking through nonpartisan research, education and engagement. KHI believes evidence-based information, objective analysis and civil dialogue enable policy leaders to be champions for a healthier Kansas. Established in 1995 with a multiyear grant from the Kansas Health Foundation, KHI is a nonprofit, nonpartisan educational organization based in Topeka.