The Growing Consequences of Inadequate Health Insurance

10 Min Read

Jan 01, 2009

By

Andrew Ward, Ph.D, M.P.H.,

Sharon T. Barfield, M.S.W., LSCSW,

Gina C. Maree, M.S.W., LSCSW

Key Points

Approximately 25 million individuals in the United States are underinsured and their numbers have increased significantly in recent years.

Medical debt is the primary cause of approximately half of all bankruptcy filings in the U.S.

In 2007, 41 percent of working-age adults in the U.S. had trouble paying their medical bills or had medical debts.

From 2002–2006, approximately 500,000 adult Kansans, who were insured, did not seek needed medical care due to cost.

Insured individuals with medical debt are three times more likely than those without debt to postpone or forgo needed care or cut back on prescription medications.

Rural residents and other consumers who purchase health insurance in the individual and small group markets are more likely to be underinsured than those in larger group plans.

Background

While much attention has been devoted to addressing Kansas’ uninsured, far less has been focused on the underinsured. Because health insurance plans rarely cover all medical expenses, increasing numbers of insured adults are finding themselves unable to pay their share of the costs. Studies show that underinsured persons frequently postpone or forgo recommended health care or cut back on needed prescription medications because of costs. In addition, many incur substantial medical debt, which in extreme cases can force people into bankruptcy. Many factors are contributing to the rise in health care expenses and medical debt. Most health insurance plans require varying levels of cost sharing through deductibles, co-pays, and coinsurance. And in recent years, those out-of-pocket spending requirements have been increasing in part because of efforts by policymakers and insurance carriers to manage costs and maintain affordable premiums. In addition, plans may impose annual or lifetime payment caps, and may exclude or limit coverage for specific illnesses or treatments. Coverage exclusions due to waiting periods or pre-existing conditions may also result in out-of-pocket expenses.

A Serious Problem, with Serious Consequences

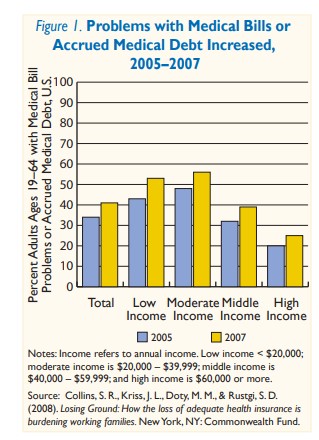

Although there is a lack of consensus on how to define and measure the prevalence of the underinsured, sufficient evidence exists to conclude that the scope of the problem in the U.S. is substantial. A recent report by the Commonwealth Fund estimated that 25 million adults were underinsured in 2007, up from 16 million in 2003. In the same study, 41 percent of working-age adults reported problems paying their medical bills or said that they had medical debt (Figure 1). Sixty-one percent of those with medical debt said they were insured when the debt was incurred. In the past five years, studies have shown an increase in the underinsured rate and significant declines in the adequacy of coverage for middle-class, working families. Additional research found that rural residents and other consumers who purchase health insurance in the individual and small group markets are more likely to be underinsured than those in larger group plans. In general, medical debt is a problem for middle-class families. A sizable majority of privately-insured adults with medical debt — 78 percent — hold fulltime jobs. One study found that these individuals were three times more likely to skip recommended tests or treatments due to costs, twice as likely to not fill prescriptions and four times more likely to postpone care than privately insured individuals without medical debt. Medical debt also contributes to credit card debt, home forfeiture and reduced access to credit. Two-thirds of families who reported problems paying medical bills also struggled to afford other necessities, such as housing, transportation and food. A recent study of bankruptcies in the U.S. found that approximately half could be traced back to serious medical problems resulting in medical debt. In some cases, underinsured individuals do not have access to the same safety net of their uninsured counterparts because having insurance — adequate or not — disqualifies them from free care.

Scope of the Problem in Kansas Difficult to Measure

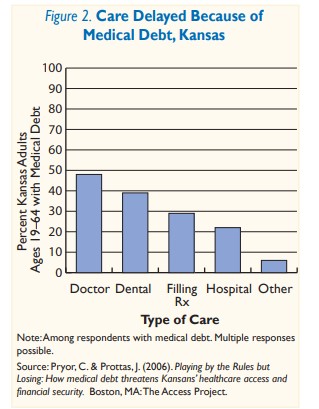

Although the number of under-insured Kansans cannot be quantified due to limited state-specific data, there are indications that inadequate coverage is a problem for many in the state. In surveys conducted from 2002–2006, more than half a million insured Kansans said they did not seek needed medical care due to cost. A 2006 study conducted by The Access Project and Brandeis University surveyed more than 1,000 patients at Kansas community health centers regarding their families’ insurance status and medical debt. This study found that medical debt was a problem for insured families, even when everyone in the family was covered. Not only did more than half of the families report having medical debt, 48 percent said they had delayed medical care because of it (Figure 2) and 52 percent said it had made paying for housing dif. cult. Many also said they had been forced to borrow money to pay their bills.

The same research organizations also conducted a survey of almost 300 Kansas farm families in 2005 and found that although 95 percent were insured, 17 percent reported having medical debt. This percent is even higher — 29 percent — when the families are non-elderly.

The University of Kansas conducted a small study in 2005 to gain a more personal understanding of the consequences of being underinsured. Researchers interviewed a sample of fifteen underinsured Kansans. Some said they had exhausted lifetime savings to pay medical bills. Others said they had lost homes or had been forced to fi le bankruptcy. Also, many of those interviewed said both they and family members had delayed or gone without recommended medical care or cut back on their prescription medications because of cost concerns. Some also reported that they had difficulty qualifying for credit and paying for housing. For these Kansans and many others like them, having health insurance was not sufficient to protect them from unaffordable health care expenses.

The Challenge of Defining and Measuring the Underinsured

One of the biggest challenges to understanding the prevalence of the underinsured is the lack of agreement on a definition and approach to measurement. Although defining and measuring the underinsured is challenging, many agree that out-of-pocket medical expenses and adequacy of health insurance benefits are important factors to consider. To date, researchers have taken various approaches:

Medical Expenses

One frequently used approach is to count as underinsured those individuals who were insured for the full year, but reported at least one of the following:

Out-of-pocket medical expenses equal to 10 percent or more of household income

Out-of-pocket medical expenses equal to or greater than 5 percent of income if the household income is below 200 percent of the Federal Poverty Level

Health plan deductibles equal to or exceeding 5 percent of the household income.

Some studies have assessed an individual’s risk for spending a defined percent of annual income on health care, while others count the numbers of insured patients who report delaying or not getting recommended health care due to cost concerns.

These approaches have limits because there is little consensus on what level of out-of-pocket medical expense is both adequate and reasonable. Measurement of expenditures incurred for health care services is likely to underestimate rates of underinsurance, because it fails to capture “non-users” of health care services. Nonusers may have good health and not yet need medical care or may have postponed or not sought care due to cost concerns. Within this array of approaches, further variations exist, such as whether insurance premium costs are included in the total expenditure tally and whether Medicare-aged adults should be considered.

Adequacy of Health Insurance Benefits

Some studies de.ne and measure the underinsured based on the adequacy of their health insurance coverage compared to a pre-established set of benchmark benefits. Others measure the individual’s perception of the adequacy of his/her health insurance benefits.

Attempts to de.ne and measure the underinsured by assessing the adequacy of a bene.t package is complicated by the lack of consensus on a standard minimum benefits package and on what constitutes “adequate” coverage. Using consumer surveys to measure the adequacy of insurance coverage is problematic because consumers often do not know whether their plan is sufficient until they have an acute or chronic health problem.

As illustrated above, there is not a perfect approach to defining and measuring the underinsured. This lack of agreement in an approach can result in policy discussions being derailed by debate over the definition and measurement of the underinsured. Therefore, both a common definition of the problem and means of measuring it are needed to ensure that policy discussions remain focused on the challenges faced by the underinsured and the policy options for addressing them.

Implications

Studies indicate that the number of underinsured in the U.S. is growing and that increasing numbers of insured families are incurring medical debt. Studies also con.rm that people don’t seek or receive needed health care when they are underinsured and concerned about medical debt. Although the scope of the underinsurance problem in Kansas is unknown, it is clear that many insured Kansans are postponing or foregoing recommended care because of cost. In addition, high health care costs and medical debt are causing financial problems for some Kansans, up to and including bankruptcy.

As policymakers seek to address the increasingly urgent issues of rising health care costs and growing numbers of uninsured, they may be tempted to focus on options that attempt to make insurance premiums more affordable by increasing out-of-pocket expenses and reducing the number of required benefits. Policy options like high-deductible plans, increasing minimum co-pays, and reducing bene.t mandates for small businesses and young adults might help to reduce health care expenditures and the number of uninsured, but they could also increase the number of people with inadequate insurance — the underinsured. These people, including many Kansans, could find themselves paying for insurance they can’t afford to use. As policymakers face challenging health policy decisions, they should carefully consider the adequacy of proposed insurance options and the potential unintended consequences of shifting costs to consumers.

Acknowledgments

Funding for this project was provided by:

The Health Care Foundation of Greater Kansas City — Providing leadership, advocacy and resources that eliminate barriers to quality health for the uninsured and underserved in our service area.

The Kansas Health Foundation — A private philanthropy dedicated to improving the health of all Kansans. For more information about the Kansas Health Foundation, visit www.kansashealth.org.

The REACH Healthcare Foundation — A nonpro.t charitable organization dedicated to improving access to quality health care for poor and medically underserved people.

The Sunflower Foundation: Health Care for Kansans — A Topeka-based philanthropic organization with the mission to serve as a catalyst for improving the health of Kansans.

The United Methodist Health Ministry Fund — A foundation based in Hutchinson with the following mission: “Healthy Kansans through cooperative and strategic philanthropy guided by Christian principles.”

The Wyandotte Health Foundation — A private charitable organization located in Kansas City, Kansas, that has this mission: “To promote and improve the health of Wyandotte County citizens, particularly the indigent, through grants and collaborative efforts.”

About Kansas Health Institute

The Kansas Health Institute supports effective policymaking through nonpartisan research, education and engagement. KHI believes evidence-based information, objective analysis and civil dialogue enable policy leaders to be champions for a healthier Kansas. Established in 1995 with a multiyear grant from the Kansas Health Foundation, KHI is a nonprofit, nonpartisan educational organization based in Topeka.