To cover as many low-income workers as possible, HNY includes a number of eligibility restrictions, most aimed at small employers. Enrollees must work for firms of 50 employees or less and at least 30 percent of these employees must earn $35,500 or less per year. In addition, the firm must not have had a comprehensive group plan available within the last year. This requirement is designed to make certain that enrollees are those who were previously uninsured and prevent “crowd out,” in which public insurance replaces policies that were bought in the private market.

Similar to the eligibility restrictions on small groups, sole proprietors or individuals must have income at or below 250 percent of the Federal Poverty Level (FPL)3 and cannot be eligible for Medicare or have had access to an employer-based health plan within the last year. All health maintenance organizations (HMOs) in the state must participate in HNY and almost everyone covered by the program is enrolled in one of these HMOs.

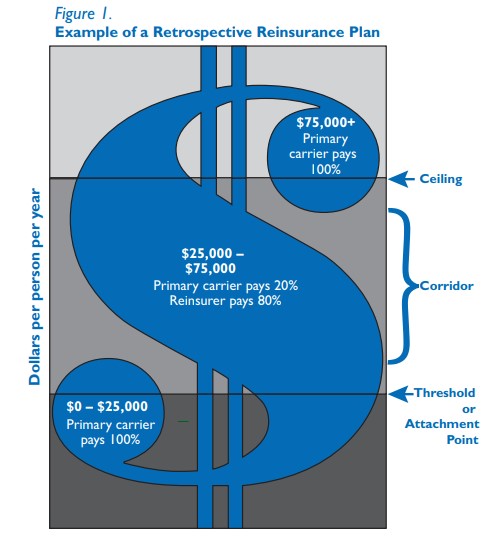

HNY initially paid 90 percent of claims between $30,000 and $100,000 and primary insurers paid 10 percent. Primary insurers were fully responsible for expenses below the $30,000 threshold and above the $100,000 ceiling. This structure resulted in premiums that were 15 percent to 30 percent lower than premiums in the small group market and about one-half of premium costs in the individual insurance market.

In the first two years of the program there were very few claims above $30,000 because most of the enrollees were relatively healthy. As a result, the reinsurance threshold was lowered to cover 90 percent of expenses between $5,000 and $75,000. This change resulted in an additional 17 percent reduction in premiums and by 2004, HNY premiums were 40 percent lower than average small group HMO premiums and two-thirds lower than premiums in the individual market.

In 2005, HNY was estimated to cost $61.7 million for 107,000 enrollees, a subsidy of about $577 per person. By the end of 2006, close to 133,000 people were enrolled in the program, including more than 10,000 small businesses, about 13,000 sole proprietors, and over 56,000 individuals.

Arizona

The Arizona Healthcare Group (HCG) was created in 1986 to help small employers (50 employees or fewer) and political subdivisions obtain health coverage. Groups qualify for the program if they have not offered health insurance coverage for at least 180 days. HCG is operated by a division of the Arizona Health Care Cost Containment System, the state’s managed care based Medicaid program. For most of its history, only HMO plans were offered to enrollees, but in 2005 a Preferred Provider Organization (PPO) option was added to the program.

HCG takes a different reinsurance approach to the risks faced by insurers than HNY. Rather than protecting insurers from unusually high costs incurred by individuals, as in New York, HCG protects insurers from high costs that may be caused by a large number of enrollees that have above average, but not extraordinary, expenses. The HNY approach provides a reservoir of funds that are used as a backup payment source for high-cost cases. As a result, insurers don’t have to build such reserves into their premiums and premiums can be set at lower levels. HCG’s approach to lower premiums entails subsidizing the higher-than-average expenses of all enrollees collectively.

HCG makes reinsurance or “stop-loss” payments to plans that experience high costs compared to premium revenue. The program is designed to ensure that medical claims costs for each plan are kept between about 80 to 86 percent of premiums. Stop-loss payments are made to plans with higher loss ratios and “stop-gain” payments are made by plans that experience lower loss ratios. At times, the reinsurance plan has been subsidized by the state, but these subsidies were ended in 2006. Other revenue to support the program comes from withholding a portion of the premiums of the primary insurers. HCG also purchases private reinsurance to cover annual losses that exceed $100,000 per enrollee.

As of December 2005, there were 18,000 individuals enrolled in HCG, an increase of more than 40 percent from the previous year. Almost all HCG enrollees are from small businesses and almost 6,000 businesses participate.

New Mexico

The New Mexico Health Insurance Alliance (HIA) was created in 1994 to reinsure small groups and sole proprietors. Enrollees must work for a firm with fewer than 50 employees and at least 50 percent of eligible employees must enroll in the program. Employees must work at least 20 hours per week before they and/or their dependents are eligible.

Like HCG in Arizona, New Mexico’s reinsurance program protects insurers through an aggregate loss system, paying out when total claims exceed 75 percent of premium revenues. HIA is funded through enrollee premium surcharges. The program sets a 5 percent premium surcharge during the first year with an increase up to 10 percent in renewal years for small groups. Individuals may have up to a 10 percent premium surcharge in their first year of coverage and up to 15 percent in renewal years. HIA balances funding deficits by having insurance carriers pitch in to cover expenses that exceed collections from premium surcharges. In 2003, New Mexico insurance carriers spent about $4.5 million to cover reinsurance losses. As of 2004, HIA had enrolled approximately 4,000 people, of which 35 percent were sole proprietors.

Idaho

Idaho’s reinsurance plan, the Small Employer Health Reinsurance Program (ID-SEHRP), was established in 1994 to cover small groups (2–50 employees). Under ID-SEHRP, small group insurers are given 60 days from issuance of a policy to decide whether to reinsure the entire group, an individual employee or an eligible dependent. Insurers’ decisions to reinsure may not be based on actual claims experience within this 60 day period.

Under ID-SEHRP, primary insurers pay premiums for each reinsured person and the state assesses all insurers to fund any losses in the program. Primary insurers are responsible for the first $12,000 of claims and 10 percent of each of the next $13,000 for enrollees in the basic plan, $88,000 for enrollees in the standard plan, and $120,000 for enrollees in the catastrophic plan. As of April 2004, 44 small group plans were reinsured under the program.

In 2001, Idaho created the Individual High-Risk Reinsurance Pool to reinsure four “high-risk pool plans” that all non-group insurers must offer. Under this plan, the primary insurer is responsible for the first $5,000 in claims costs and 10 percent of costs from $5,000–$25,000. The reinsurance pool covers 90 percent of costs in the $5,000–$25,000 corridor and all claims above this amount. This plan is funded with reinsurance premiums from insurers and, if these premiums are not sufficient to cover all claims, with supplemental funding from the state premium tax. As of 2004, the Individual High-Risk Reinsurance Pool had 1,358 enrollees.

Connecticut

Connecticut’s Small Employer Health Reinsurance Pool (CT-SEHRP) was established in 1990 and has been used by the National Association of Insurance Commissioners (NAIC) as a model for a state reinsurance program. CT-SEHRP reinsures all insurance carriers in the state that write policies for small groups (less than 50 members). As in Idaho, insurers have 60 days from issuance of a policy to designate individuals or entire groups for reinsurance. Only permanent employees who work more than 30 hours per week and their dependents are eligible for reinsurance.

Primary insurers pay a $5,000 deductible for each reinsured life and the pool pays for all claims above that amount. Funding for the reinsurance pool comes from premiums paid by the insurers who cede risk to the pool and an annual assessment on all carriers in the state, based on market share. Assessments are limited to an annual maximum of one percent of an insurers’ small group premium base, but have never reached that level. As of October 2004, more than 3,000 individuals were enrolled in the program at an average reinsurance premium of $4,500 per year.

What Issues are Important in Design of a Reinsurance Program?

Policymakers must be aware of a number of issues in designing a reinsurance program. Factors such as who the program will cover, how it is structured and the sources of funding must be carefully considered within the context of the state’s regulatory and political environments. Following is a discussion of these issues.

Who will it cover?

The groups and individuals that will be covered by a reinsurance program will to a large degree dictate the design of the program and its cost. States must ask the following questions:

-

- Who will be reinsured? Possible targets include small groups (e.g., businesses with 2–50 employees), sole proprietors, and/or individuals.

- Will reinsurance be available for all members of the group or only those who meet certain qualifications? The HNY plan in New York, for example, limits employer eligibility to small businesses with a certain proportion of relatively low-wage workers.

- What requirements will be placed on those being reinsured? The program may require certain levels of employee participation and periods of uninsurance. The New Mexico HIA program, for example, requires 50 percent of eligible employees in a group to enroll and only employees who work at least 20 hours per week and/or their dependents are eligible. HCG in Arizona limits eligibility to groups that have not offered health insurance coverage for at least 180 days.

- Will all or only some enrollees be reinsured? In New York, Arizona, and New Mexico, all enrollees are reinsured. In Idaho and Connecticut, on the other hand, the primary insurer selects which enrollees to reinsure.

How will it be structured?

The basic framework of a reinsurance plan will have a direct impact on its cost and effect on the market. Policymakers must first decide whether to reinsure against high aggregate insurer losses (as in Arizona and New Mexico) or high losses from individual enrollees (as in New York).

Aggregate loss programs are more successful at increasing market competition by enabling newer insurers with fewer enrollees to set competitive premiums. There is a risk under an aggregate loss reinsurance program, however, that some insurers will set premiums too low and become dependent on reinsurance to stay financially viable. Plans that reinsure against the high claims costs of individual enrollees, known as “market stabilization” plans, are better at encouraging insurers to control enrollee costs. It is possible, as well, to design a reinsurance plan that shares aspects of both types of programs.

Another fundamental consideration is the design of payment responsibilities — the threshold at which the reinsurer will assume an obligation for covering claims, the ceiling at which the reinsurers’ responsibility ends, and the percentage of expenses within the corridor that will be covered by the primary insurer and the reinsurer.